How Liquidity Depth Behaviour Shapes Execution Across Venues

Liquidity depth behaviour shapes how systematic engines move capital through real markets. It reveals the difference between a quoted price and a price an engine can actually fill. For institutional infrastructure, this distinction matters more than any single signal. Depth is not a number on a screen. Instead, it acts as a behavioural property of a venue. Participants, mechanics, and session timing all shape it.

Most retail frameworks treat liquidity as a fixed background condition. By contrast, systematic infrastructure treats it as a live property that changes by venue, regime, and session. Furthermore, depth in ASX large caps behaves differently from depth in US large caps. Understanding these differences is not a stylistic preference. It functions as a structural requirement for engines that operate across markets.

This article examines liquidity depth behaviour as a cross-venue property. Specifically, it covers what depth measures, how it shifts across exchanges, why it matters for execution, and how disciplined systems engineer around it. As such, the framework here follows a behaviour-first approach. Structure first, prediction never.

What Liquidity Depth Behaviour Actually Measures

Depth is one of the most misunderstood properties in markets. Many traders see it as the bid-ask spread or top-of-book size. In reality, liquidity depth behaviour describes how the order book responds to demand across price levels over time. It captures shape, refresh, and reliability as a single behavioural signal.

Liquidity depth behaviour as a structural property

Liquidity depth behaviour is not a snapshot. Instead, it represents a sustained property of the order book under load. A book may look thick at a single point in time and prove fragile under pressure. Equally, a book may look thin and yet refill consistently within milliseconds. The structural reading captures both static and dynamic dimensions. In particular, it focuses on how the book regenerates after each interaction.

For systematic engines, structure matters more than instantaneous appearance. A venue with reliable refresh patterns gives engineering teams a stable execution surface. By contrast, a venue with spiky, irregular depth produces unpredictable slippage. Therefore, depth must be read as a behaviour, not a single quote.

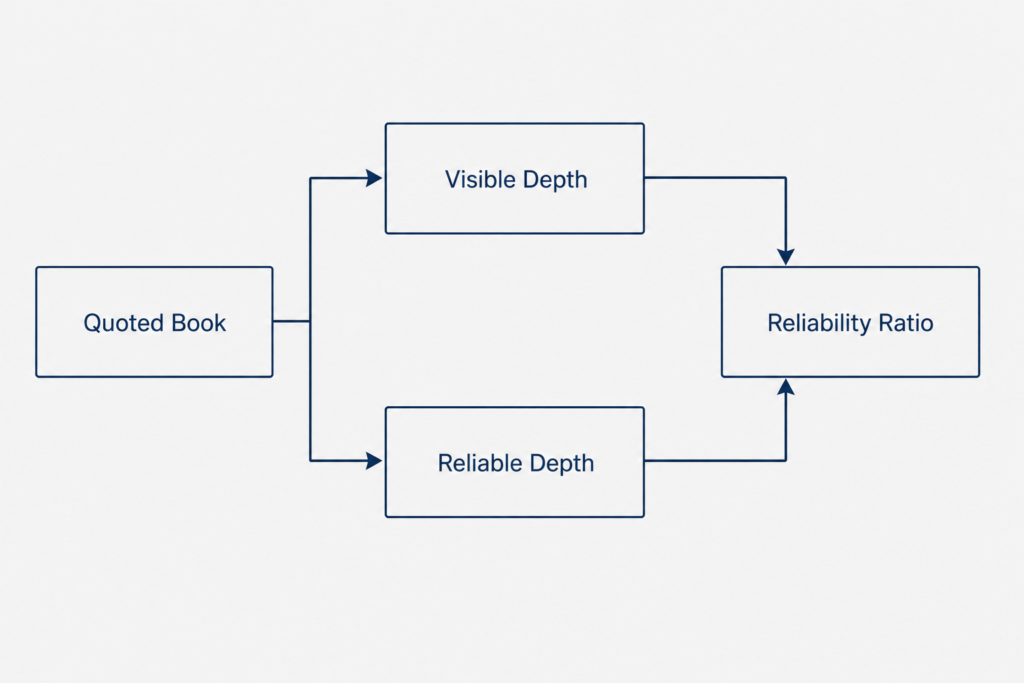

Visible versus reliable depth behaviour

Visible depth is what shows on the screen. Reliable depth is what actually fills when an order arrives. The gap between these two can be wide. In modern markets, many orders sit in the book briefly before cancellation. Consequently, visible size often overstates true execution capacity.

Systematic infrastructure must distinguish the two. The simplest measurement compares quoted size to filled size when the price is probed. Over many observations, a clear pattern emerges per venue. Some venues consistently fill close to their quoted size. Others routinely deliver only a fraction. As a result, the reliability ratio becomes a venue-level constant that informs sizing decisions.

Why raw volume hides the structural read

Daily volume is a popular liquidity proxy. However, it is a misleading one. A stock can trade billions of dollars per day and still have a fragile book at any specific moment. Volume captures throughput across the entire session. Depth behaviour captures available capacity at the point of decision.

The distinction matters most when engines size positions. By design, a behaviour-first system reads depth at the moment of intent. As a result, sizing reflects the venue’s real-time conditions, not its average historical profile.

Liquidity Depth Behaviour Across Continuous Sessions

Continuous trading is where most institutional engines operate. The continuous session has its own depth signature for every venue. As such, reading liquidity depth behaviour across continuous sessions becomes essential for cross-market design.

ASX continuous session profile

The ASX runs a single primary exchange model with concentrated order flow. Top 200 names show deep, stable books during the core session. By contrast, mid-cap and small-cap names display thinner depth with wider spreads. Spreads tighten through mid-morning as institutional flow arrives. Furthermore, they often widen again in the final hour as participants reduce inventory before close.

Depth profile in ASX large caps tends to be more uniform across the session. Liquidity providers operate with longer queue tolerance because venue fragmentation is low. As a result, refresh rates are slower than US large caps but more predictable. Engineers reading this profile build sizing logic that respects the slower regenerative rhythm.

US large-cap order book structure

US large caps trade across many venues simultaneously. NYSE, Nasdaq, BATS, IEX, and dozens of dark pools share flow. The aggregate national best bid and offer reads thicker than any individual venue. Consequently, aggregate depth becomes a routing question, not just a venue question.

Refresh rates are faster in US large caps. Latency advantages produce intense queue competition. Hidden liquidity is more prevalent. In addition, the closing auction has grown into the single largest concentrated event of the day. These factors shape a different liquidity depth behaviour from ASX continuous trading.

Cross-venue asymmetries in depth behaviour

A given notional size produces different impact across venues. The same five million dollar order behaves one way in an ASX top 50 name and another in a US S&P 500 constituent. Decay patterns differ. Recovery times differ. Therefore, engines that work cleanly in one venue may not transfer without recalibration.

Recognising these asymmetries is engineering, not preference. The granular case for microstructure variance across regions illustrates how the same nominal flow produces distinct behavioural outcomes by market. In practice, the core algorithm stays constant. Only the depth model changes by venue.

Why Liquidity Depth Behaviour Matters for Systematic Engines

Depth is not abstract for systematic infrastructure. It directly informs sizing, slippage, and risk gating. The three connect into a single discipline.

Order sizing and depth behaviour

Order size is a function of available depth, not target allocation. A position concept may call for a five percent portfolio allocation. However, if depth permits only a fraction at acceptable impact, the engine must size down. As such, the depth read becomes a binding constraint on intent.

Static sizing breaks under regime change. A rule that says “trade 100,000 shares” works only while depth holds. When depth contracts, the same order produces unacceptable slippage. Therefore, sizing logic must reference live depth observation rather than fixed quantity rules.

Slippage as venue-dependent depth behaviour

Slippage is not random. It is a structural property of how depth reacts to demand. Different venues produce different slippage distributions for the same notional. Models that ignore this end up overestimating profit and underestimating cost.

For example, slippage in ASX mid-caps tends to show heavier tails than slippage in US large caps. In addition, the slippage profile changes by time of session. Modeling slippage well means modeling liquidity depth behaviour at the venue level.

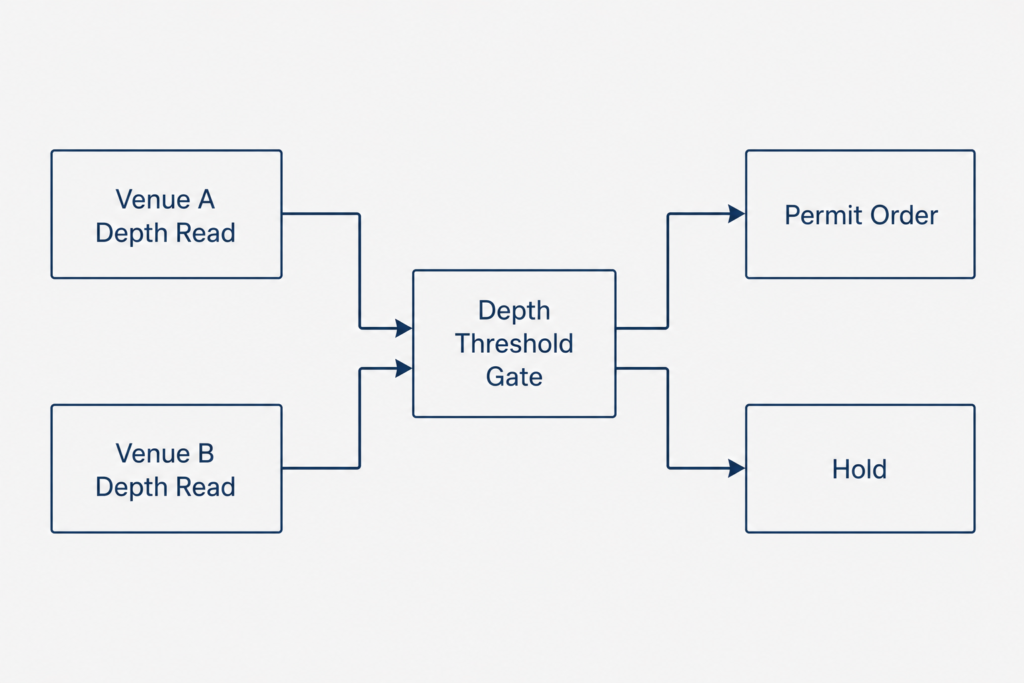

Risk gates informed by liquidity depth behaviour

Permission to enter a position depends on observed depth conditions. If depth fails to meet a defined threshold, no trade enters. This is risk-first design at the execution layer. Furthermore, it makes depth a gating variable rather than a footnote.

A behaviour-first engine treats depth as a permission. The same logic that allows entry on calm depth holds back entry on degraded depth. Consequently, the system trades less in poor conditions, not more. In practice, this restraint is structural, not discretionary.

Auction Mechanics and Liquidity Depth Behaviour

Continuous sessions tell most of the story. However, the auction phases at open and close behave differently from continuous trading. As a result, engines need a separate read for each.

Opening auction signatures

The opening auction is a single price-discovery event. Indicative price and volume build through the pre-open period. Watching this build provides insight before the continuous session begins. Furthermore, the build pattern reveals participation across the order book.

A clean build with thick indicative volume signals stable opening conditions. A chaotic build with rapidly shifting indicative price signals contested opening. Systematic engines that read this signature gain calibration before placing first orders.

Closing auction depth behaviour

The closing auction has become the largest concentrated event in many markets. In US large caps, closing volume routinely exceeds twenty percent of the day’s total. ASX market-on-close volume has grown similarly over the past decade. As a result, the close concentrates risk and opportunity in a narrow window.

Closing depth reads differently from continuous depth. Participation is institutional, often passive and benchmark-driven. Refresh dynamics are constrained by auction mechanics. In addition, the auction print is a single number rather than a continuous discovery process. Engines that handle closes must model this distinct regime.

Reading auction and continuous separately

High auction depth does not imply strong continuous depth. Closing auctions concentrate participation that did not exist during the day. Treating auction prints as a continuous depth indicator misleads sizing decisions. Consequently, the two regimes must be read separately.

A practical rule: auction observations inform auction operations only. By contrast, continuous depth observations inform continuous operations. In practice, mixing the two corrupts the venue model.

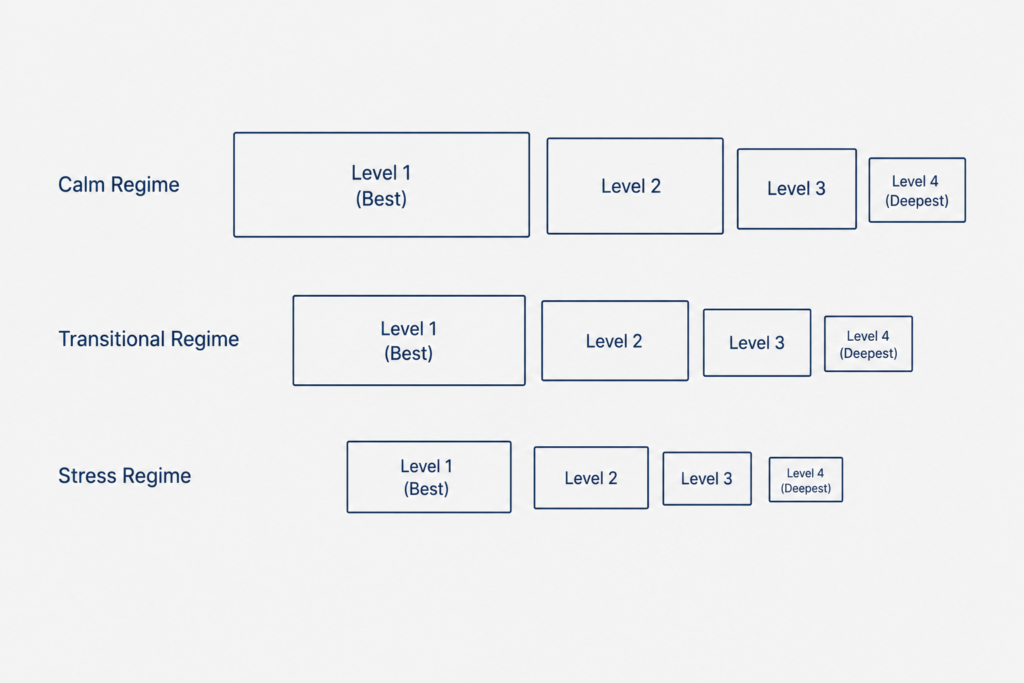

Stress Regimes and Liquidity Depth Behaviour

Calm conditions tell you what depth looks like. Stress conditions tell you what depth actually is. The difference is critical for systematic design.

Refresh rate as early stress indicator

Stress is when uncertainty rises faster than information. Liquidity providers respond by widening, thinning, or withdrawing. Depth that looked stable in calm conditions becomes patchy. Furthermore, refresh rates slow as algorithms reassess risk.

The first warning is usually refresh rate degradation. Quotes still appear, but they refresh more slowly. Engines that monitor this dimension see stress before it reaches headline volatility. As such, refresh telemetry becomes an early indicator.

Stress reveals true liquidity depth behaviour

Stress is the venue’s behavioural truth. Calm markets allow fragile structures to look adequate. Under stress, what is structural endures. What is decorative dissolves. This filter is why systematic engines must observe across regimes, not just average conditions.

A book that sustains depth through volatility expansion is qualitatively different from a book that thins on the first shock. The same nominal size means very different things in the two cases. Therefore, depth observation must include stress windows as core training input.

Venue stress responses across regions

Different venues respond to stress differently. The ASX uses volatility halts and tick-size adjustments. US markets use limit up and limit down bands plus individual stock halts. Each design produces a different stress profile.

Consequently, a depth model calibrated for one venue does not translate cleanly to another in stress. Cross-venue engineering must encode each venue’s stress mechanics as a separate parameter set. In practice, this is the architectural cost of operating across markets.

Engineering Discipline Around Liquidity Depth Behaviour

All of the above is observation. The discipline begins when observation becomes structure. Engineering turns liquidity depth behaviour from a measurement into a control surface.

Filtration gates and entry permission

Filtration logic decides whether a candidate setup is tradeable. Depth telemetry is one of its core inputs. If observed depth fails to clear thresholds, the setup never reaches the order layer. As such, filtration encodes what makes a venue tradeable in real time.

This is not a discretionary judgment call. It is a deterministic gate. The same conditions produce the same decision every time. Consequently, engine behaviour stays consistent across operators and sessions.

Calm execution through stable depth behaviour

Calm execution is a system output, not a personality trait. Engines that trade only when depth is stable produce calm execution by design. The behaviour of the engine inherits the behaviour of the chosen environment. In particular, restraint during poor depth conditions is what produces stability during good ones.

A noisy engine trades through every environment. A disciplined engine trades only where its depth model holds. Therefore, calm output reflects the integrity of the filtration layer, not luck.

Operational reading of depth behaviour

Operational discipline means real-time monitoring of depth health. When depth degrades below threshold, the system pauses entries. When stability returns, entries resume. This loop is automated, not discretionary.

Operators do not override the gate based on intuition. By design, the system pre-commits to a rule that does not bend under pressure. In this way, depth telemetry becomes part of the operational core, not a peripheral metric.

Reading the Venue as a Behaviour, Not a Number

Markets are easier to talk about as numbers. However, they trade as behaviours. Liquidity depth behaviour is the most direct expression of this distinction in execution. Quoted depth is the number. Refreshed, reliable, regime-aware depth is the behaviour.

Across ASX continuous trading, US large-cap structure, opening and closing auctions, and stress regimes, depth carries different signatures. Engines that respect these differences build infrastructure that survives across venues. Engines that ignore them inherit fragility.

This framing is not about prediction. By contrast, it is about reading the structural surface accurately and engineering around it with discipline. Behaviour first, structure first, prediction never.

Continue learning about systematic behaviour frameworks. Follow the upcoming series on structure-first system design for further reading on venue calibration, filtration logic, and operational discipline.

About the Author

Dovest is a systematic trading infrastructure company based in Australia. Our research focuses on behaviour-first engineering: building engines whose performance stays stable, explainable, and auditable under real-world conditions. Our framework treats structure, filtration, and risk architecture as the primary objects of design. Signals are downstream of behaviour, never the other way around.

Disclaimer

This article is research and educational content. It does not constitute investment advice, a recommendation to trade, or a solicitation of any kind. Past performance does not guarantee future results. Readers should consult appropriately licensed professionals before making investment decisions.