Why Microstructure Variance Across Regions Drives System Design

Cross-border systematic trading looks deceptively uniform from a dashboard. However, the infrastructure beneath each regional market carries its own rules, timings, and behavioural signatures. The concept of microstructure variance across regions captures that structural gap. Specifically, it describes how order books, auction mechanics, halt thresholds, tick regimes, and data pipelines each carry a regional fingerprint. For institutional trading infrastructure, this variance is not a nuance. Instead, it determines whether an engine scales cleanly or drifts silently when it crosses a border.

At Dovest, microstructure variance across regions sits inside the first layer of environment-based reasoning. Therefore, engineers treat every region as a distinct behavioural surface with its own contracts. As a result, filtration, permission, and execution logic adapt to local structure without losing system identity.

Moreover, allocators now probe cross-border discipline more closely. In practice, regional depth asks a simple question: does the engine understand where it trades, or does it assume global uniformity? This article maps the structural sources of regional variance. Furthermore, it explains how systematic infrastructure absorbs each source as explicit governance input. As such, the framing stays close to engineering discipline rather than discretionary narrative.

What Microstructure Variance Across Regions Means in Practice

Microstructure is the ruleset that governs price formation at the finest level. These rules include order priority, tick size, venue fragmentation, auction timing, halt thresholds, and fee design. Regional regulators set these rules independently. Consequently, the same asset class behaves differently in the United States, Europe, Japan, Hong Kong, and Australia.

Microstructure variance across regions is the structural gap those choices produce. Importantly, that gap shapes outcomes that look identical on a price chart. For this reason, a systematic engine that ignores the gap will misread execution quality, depth behaviour, and stress response.

Regional microstructure as a structural input

Systematic infrastructure depends on repeatable behaviour under varied conditions. Therefore, the environment around the engine must enter the framework as explicit input. Regional microstructure forms part of that environment. As such, it belongs in code paths and governance logs rather than in assumptions.

By contrast, global-only logic treats markets as one surface. Such logic assumes rules rhyme closely across borders. In practice, they rarely do. As a result, execution outcomes drift in ways the global model cannot attribute.

The distinction matters for governance. Specifically, explicit regional modelling allows clean root-cause analysis when behaviour shifts. Moreover, it separates environmental change from model drift, which preserves diagnostic clarity under stress.

Why microstructure variance across regions resists smoothing

Some frameworks treat regional differences as noise to average out. However, smoothing hides drift. In particular, execution quality degrades when a model expects behaviour the venue cannot produce. Therefore, the variance must register as structured input, not residual error.

Furthermore, smoothing weakens monitoring signals. Consequently, the team loses the ability to tie behavioural change to a structural shift in one region. In this way, regional awareness protects the audit trail institutional review demands.

Encoding regional microstructure as behavioural contracts

Each region carries a behavioural contract that the engine checks at runtime. Specifically, the contract records expected depth behaviour, halt response, session boundaries, and fee treatment per venue. As a result, the engine can flag deviations before risk accumulates.

Moreover, the contract acts as documentation. Allocators, risk reviewers, and engineers read the same document and reason about the system consistently. Therefore, regional discipline becomes a communication asset rather than a hidden complexity.

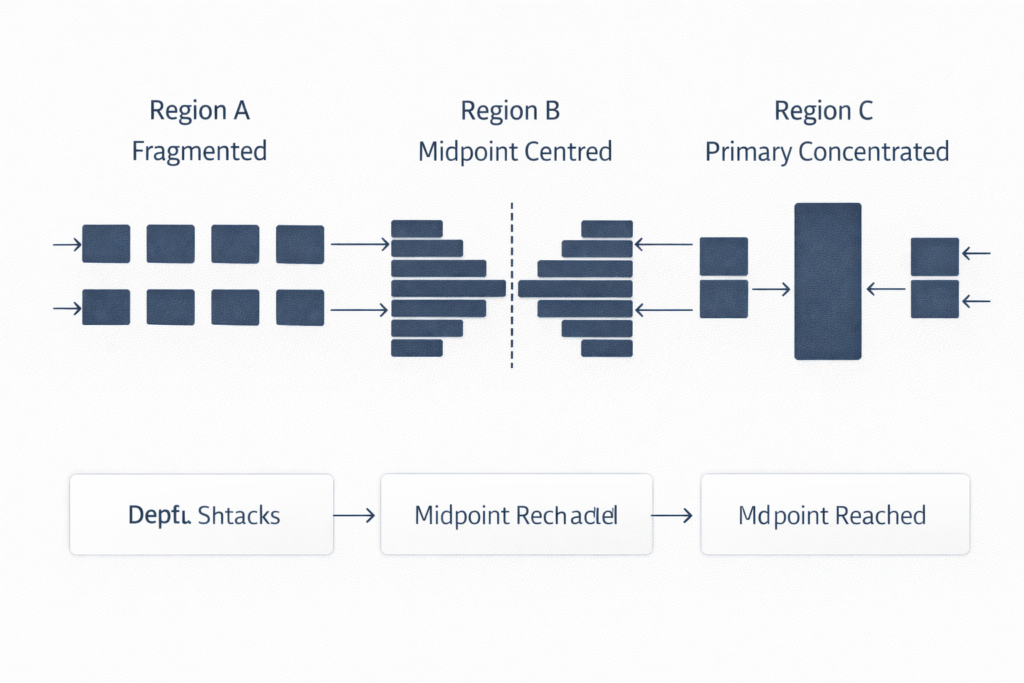

Order Book Topology Across Regional Venues

Order book topology describes the shape of displayed depth around the midpoint. However, that shape varies sharply by region. Consequently, execution logic calibrated on one topology can misjudge opportunity elsewhere.

Depth profiles under regional microstructure

US equities display deep top-of-book liquidity spread across fragmented venues. European books often show shallower top-of-book with more reliable midpoint references. Similarly, Australian books concentrate depth at primary venues with orderly retreat during stress. In particular, each signature demands its own filtration approach and queue model.

Furthermore, dark pools and alternative venues sit at different weights across regions. In US equities, off-exchange volume can exceed 40% during certain hours. By contrast, many Asian regions keep most activity on the primary lit venue. Therefore, a model assuming consistent lit share across geographies will misread execution opportunity.

Venue fragmentation and regional microstructure

Venue fragmentation describes how trading volume distributes across competing exchanges. In the US and Europe, fragmentation runs high and persistent. By contrast, Hong Kong, Tokyo, and Sydney show lower fragmentation. Consequently, routing logic must adapt or it will send orders to venues that lack the liquidity signature the model expects.

Moreover, fragmentation patterns evolve through the session. Specifically, volume often concentrates during opens and closes as flow migrates toward auction venues. For this reason, the system must model fragmentation as time-varying and region-specific rather than a static share table.

Quote intensity shaping regional microstructure

Quote intensity measures how quickly quotes update at the inside. Regions diverge here too. In particular, US inside quotes can update thousands of times per second for liquid names. Nevertheless, many Asian venues produce lower quote rates with more stable queues. Therefore, queue priority strategies effective in one region may fail to secure fills in another.

Additionally, queue dynamics interact with tick regimes. When ticks narrow, queue value declines. When ticks widen, queue priority gains weight. As a result, similar strategies produce different outcomes depending on the regional microstructure they encounter.

Session Architecture Across Regional Markets

Session architecture describes when markets open, close, pause, and reopen. These timings are not cosmetic. Instead, they shape the behavioural regime in which each decision executes.

Opening mechanics and microstructure variance across regions

The US opens with a continuous phase after a structured opening print. By contrast, European markets run longer call auctions with extended price discovery. Furthermore, Tokyo and Hong Kong use opening auctions with pre-market collection phases that carry distinct information dynamics.

These differences change how quickly price stabilises after the open. As a result, entry logic that assumes stable first-minute pricing can fail in regions where auction convergence unfolds slowly. Therefore, regional opening profiles must enter the engine as explicit regime parameters rather than hidden assumptions.

Closing concentration patterns across regions

Closing auctions carry disproportionate liquidity in many regions. In particular, European and Asian closes pack substantial volume into narrow windows. Consequently, execution models that ignore closing concentration distort risk exposure at the final print.

Similarly, derivative expiries interact with regional closes in specific ways. For this reason, filtration logic treats closing windows as separate behavioural states with tightened constraints rather than extensions of the continuous session.

Mid-session breaks and regional microstructure

Some regions introduce mid-session breaks that continuous markets do not. Specifically, Tokyo and Hong Kong run lunch breaks with reopening auctions. Moreover, certain venues invoke volatility auctions after shock events. As a result, positions held across these windows carry overnight-style risk during the break itself.

Furthermore, technology layers built for continuous markets may misread these events as feed interruptions. Therefore, the system must recognise structural pauses explicitly and mark them in the session calendar with clear handling rules.

Tick Regimes and Fee Design in Regional Microstructure

Tick policy sets the smallest price increment allowed. Fee models determine the cost of liquidity provision and consumption. Together, they shape quoting behaviour and execution economics. However, both vary substantially across regions.

Tick size regimes across regional venues

The US allows sub-penny quoting only within certain price bands. Europe applies the MiFID II tick regime with size tiers linked to liquidity. Furthermore, Japan runs asset-specific tick schedules adjusted by liquidity class.

These differences change what a one-tick move actually means. In practice, a one-tick change in one region may equal multiple ticks in another. For this reason, signal thresholds calibrated globally will misread local structure.

Moreover, tick policies evolve through regulatory review. US markets have debated sub-penny pilot programs. European regulators have refined MiFID II tick tiers multiple times. Consequently, a static tick table stored in code becomes stale without governance oversight.

Fee structures shaping microstructure variance

Fee models include maker rebates, taker charges, flat access fees, and transaction taxes. Regional venues select different mixes. Specifically, US venues favour maker-taker rebate structures. Some European venues run inverted models, while several Asian markets layer transaction taxes on top of exchange fees.

Consequently, the economics of aggressive versus passive execution differ sharply. In particular, a strategy profitable under rebate capture in the US may lose money under an Asian tax regime. Therefore, regional fee models must feed directly into permission logic, not only post-trade accounting.

Rebate dynamics and queue behaviour

Rebate structures attract specific quoting patterns. In practice, deep queues form at maker-friendly venues, while taker-friendly venues thin at the inside. As a result, similar signals receive different execution quality depending on the venue they route to.

Moreover, rebate levels shift when venues compete. Therefore, the engineering team tracks rebate changes with the same discipline as regulatory announcements. By design, regional microstructure extends into the commercial layer, not just the regulatory layer.

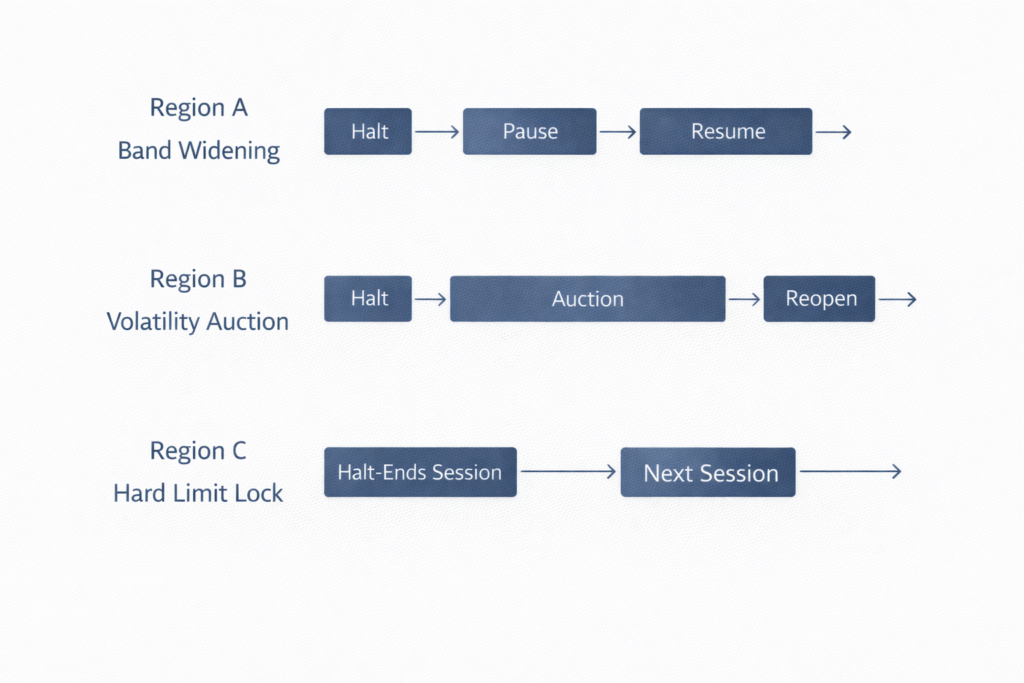

Halt Logic and Microstructure Variance Across Regions

Circuit breakers and halt mechanisms protect markets from destabilising moves. However, their design varies widely across regions. Consequently, halt behaviour is one of the most visible drivers of microstructure variance across regions.

Price collars, bands, and circuit logic

US equities use limit-up limit-down bands that widen during stress windows. European venues combine price collars with volatility auctions. Furthermore, several Asian regions apply hard daily price limits that cap movement entirely for the session.

These differences change what a halt means operationally. In some regions, halts are brief pauses that clear in minutes. In others, halts may end trading for an instrument that day. Therefore, systematic engines must interpret halt semantics region by region rather than through a universal rule.

Recovery profiles under regional microstructure

Halt recovery varies as sharply as halt design itself. Specifically, US bands adjust intraday based on reference price. By contrast, many Asian limits stay fixed for the session. As a result, post-halt discovery proceeds at different speeds.

Moreover, some regions reopen with narrow spreads and fast re-engagement. Others require extended reopening auctions with wide quotes. For this reason, re-entry logic after stress events respects regional recovery timelines rather than a single global tempo.

Hard limits and regional microstructure lockouts

Hard daily limits cap price moves absolutely. Furthermore, they can end productive trading in an instrument once a limit locks. In such cases, exits become impossible until the next session reopens. Therefore, size allocation in limit-prone regions anticipates worst-case immobilisation, not only typical slippage.

Moreover, lockouts propagate through related instruments. In particular, futures, options, and ETFs referencing a locked underlying may widen spreads or halt themselves. As a result, the engine must model cross-instrument halt propagation as a first-class regional risk. Consequently, microstructure variance across regions extends into derivative exposure, not only cash execution.

Data and Timing Variance in Cross-Border Systems

Data quality is not uniform globally. Furthermore, each region produces its own artefacts in feed structure, timestamps, and corporate action handling.

Feed precision and regional latency

Feed precision varies. Specifically, nanosecond timestamps appear in parts of the US and Europe. By contrast, some regional feeds provide millisecond precision only. As a result, cross-regional comparisons require careful alignment rather than direct subtraction.

Moreover, feed delivery paths differ. Colocation runs as standard in the US and Europe but differs in cost and access across Asian venues. Consequently, latency topology changes how quickly quotes arrive at the engine. For this reason, models calibrated on one latency regime may time entries poorly in another.

Corporate actions and regional microstructure

Corporate actions propagate through data feeds with regional lag. Additionally, splits, dividends, and rights issues apply on different schedules. Consequently, a systematic pipeline normalises these events with regional awareness, not global assumptions.

Reference data itself carries regional variance. Specifically, security master files use different identifier conventions, corporate action codings, and symbol rollover rules. As a result, joining cross-regional data without explicit regional keys produces silent mismatches that monitoring struggles to catch.

Session clocks and daylight transitions

Session boundaries map to local market time, not UTC alone. In practice, regions transition to and from daylight saving on different dates. Some regions do not observe daylight saving at all. Therefore, the ingestion layer carries a regional calendar that updates ahead of every transition window.

Furthermore, holiday calendars diverge. For example, Lunar New Year affects several Asian markets but not Western ones. As a result, session availability respects local rhythms rather than a universal calendar.

In addition, half-day sessions before holidays create partial trading windows. Specifically, abbreviated sessions shrink liquidity and shift auction weights. Consequently, size and permission logic must recognise these windows as distinct regimes rather than light versions of a full session. In this way, regional microstructure enters time-based permissioning directly, not as an afterthought in session handling.

Governance of Microstructure Variance Across Regions

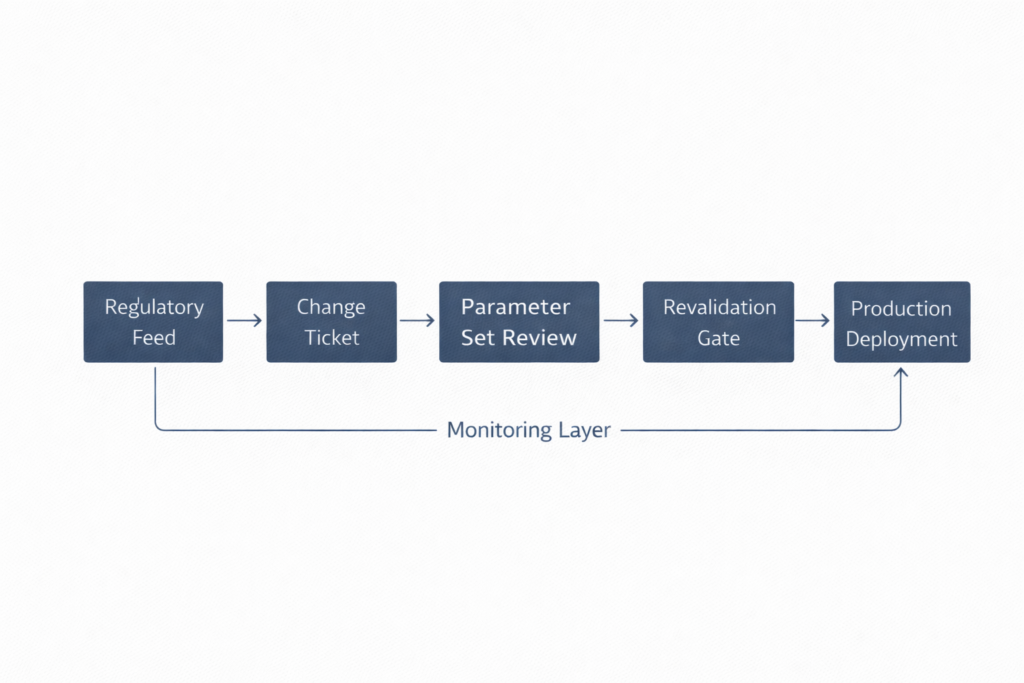

Regional microstructure is not static. Regulators change tick regimes, halt policies, and fee models over time. Consequently, governance cannot rely on one-off validation. Instead, it operates as a continuous function tied to regional cadence.

Regional parameter sets and change control

Each region carries a parameter set that governs its behavioural contract. Specifically, the set records tick schedules, halt thresholds, session calendars, and fee models. Moreover, every change to the set passes through a review gate with a documented rollback path.

In this way, no parameter shifts silently. Furthermore, the governance log records who approved each change and why. As a result, institutional reviewers audit the regional logic without interviewing engineers.

For more on pre-commitment boundaries that govern these review gates, see pre-commitment rules within systematic trading.

Regulatory cadence and revalidation

Regulators publish bulletins, venue notices, and rule changes on their own schedules. Therefore, the governance layer subscribes to regional regulatory feeds and routes events to the appropriate review path. Moreover, revalidation runs before any parameter change reaches production code.

Additionally, the layer pairs each regulatory event with a change ticket. Consequently, the audit trail connects regulator action to engineering action without narrative reconstruction.

In practice, regional cadence varies widely. Some regulators announce rule changes quarterly. Others adjust venue-level rules with short notice windows. Therefore, the governance layer scales its attention regionally rather than applying a single universal tempo. In this way, microstructure variance across regions shapes governance workflow design as much as it shapes execution logic.

Monitoring for regional microstructure drift

Monitoring checks actual behaviour against the behavioural contract. Specifically, the monitor watches depth signatures, queue recovery, halt response, and fee realisation. When observed behaviour drifts from the contract, the system raises a signal and may tighten permissions.

Furthermore, the monitor separates short-term variance from structural shift. As a result, the team decides between recalibration and full re-review. In this way, microstructure variance across regions becomes an input to continuous governance rather than a one-off study.

Regional Microstructure as an Allocator Signal

Treating regional microstructure as a design discipline changes how allocators evaluate infrastructure. In particular, it separates teams that treat global markets as one surface from teams that respect structural differences.

What allocators see in regional discipline

Allocators increasingly examine cross-border governance. Specifically, they look for regional parameter sets, change logs, and revalidation paths. Moreover, they ask how the engine behaves when a region’s microstructure shifts mid-cycle. As a result, regional discipline becomes a visible signal of institutional depth rather than an internal engineering detail.

Microstructure variance across regions as diagnostic tool

Regional awareness also reframes how teams respond to underperformance in any single region. Instead of retuning signals first, engineers check whether the region’s microstructure profile has shifted. Consequently, they distinguish between model drift and environmental change. In this way, the framework produces diagnostic clarity rather than reactive tuning.

Moreover, this discipline supports cleaner conversations with allocators, risk committees, and auditors. Specifically, they can review the regional parameter sets directly. Therefore, the dialogue moves away from opaque performance narratives and toward structural accountability. By design, this shift protects the institutional character of the framework.

Finally, regional discipline improves cross-border scaling decisions. In particular, expansion into a new region proceeds only after engineers characterise its microstructure and absorb it into the framework. As a result, the engine preserves behavioural identity across environments, not only across time. For this reason, microstructure variance across regions functions as a staging gate for responsible capacity growth.

Continue Learning

Follow the upcoming Dovest series on structure-first system design and cross-border governance.

About the Author

Dovest Research is the institutional research arm of Dovest, publishing frameworks on systematic trading infrastructure, behavioural integrity, and risk architecture. The team focuses on structure, filtration, and governance that keep trading engines stable, explainable, and auditable under real-world stress.

Disclaimer

This article is for institutional research and educational purposes only. It does not constitute investment advice, a recommendation, or an offer of any product or service. Dovest does not provide trading signals, performance guarantees, or forecasts.