Audit Standards in Systematic Trading: What Verified Behaviour Proves

Most systematic trading conversations begin with results. Win rates, monthly returns, and drawdown figures dominate the review process for most observers. However, those metrics answer only one question: did the system produce profit? They do not address a deeper and more operationally important question: did the system behave as its design intended?

Audit standards in systematic trading exist to answer that second question. They shift the frame from output to process, from results to structural behaviour. For institutional observers, audit standards in systematic trading represent the foundation for long-term trust. They create the evidence base that performance records alone cannot provide. They also separate systems that happened to perform well from systems that are structurally capable of repeating that performance under different conditions.

This article examines what audit standards must cover in practice, how verified behaviour differs from backtested logic, and why governance-first design produces institutional credibility that results-focused reporting cannot replicate.

Why Audit Standards Systematic Trading Matter More Than Performance Records

Performance records compress an entire sequence of decisions into a single output number. That compression is useful for surface comparison. However, it removes exactly the information that institutional observers most need: whether the system followed its documented logic throughout the period under review.

A system can breach its internal risk constraints and still report a positive month. It can bypass its filtration logic under market pressure and still record profitable trades. In each case, performance figures hide the structural failure because they evaluate outcomes rather than processes. Audit standards prevent that concealment. They require evidence not only of what the system produced but of how it produced it.

The Limits of Performance-Only Review

Performance-only review produces a particular kind of blind spot. It creates confidence in systems that behaved correctly during favourable conditions but have not yet encountered the stress states that reveal structural weaknesses.

A system running in a low-volatility, trending market environment may produce strong results through a combination of adequate position sizing and benign conditions. That result does not confirm the system is robust. It does not confirm the system will maintain its behaviour when liquidity compresses, when volatility spikes, or when a regime shift removes the conditions the system was implicitly relying on.

Furthermore, performance-only review gives no insight into how close the system came to violating its risk constraints. A system that stayed within its limits by a narrow margin during a stress event represents a very different risk profile than one that maintained wide structural headroom throughout. Audit standards capture that distinction. Performance records do not.

How Audit Standards Systematic Trading Reframes the Review Question

Audit standards in systematic trading reframe the central review question. Instead of asking whether the system made money, they ask whether the system did what it was designed to do. That shift has immediate practical consequences for how institutional observers evaluate long-term risk.

A system that produced returns while violating its own exposure limits is not institutionally trustworthy. It is a system that operated outside its intended structure and happened to be rewarded for it. By contrast, a system that followed its documented rules consistently, even through drawdown periods, has demonstrated genuine structural discipline. Audit standards make that distinction visible. Performance records make it invisible.

Consequently, institutional review processes that rely on audit standards produce a different quality of evidence. The evidence they generate is operational, not statistical. It addresses whether the system behaved correctly, not whether the market rewarded it.

What Verified Behaviour Reveals in Systematic Trading

Verified behaviour provides a different form of institutional evidence than backtested logic or observed performance. It shows how the system responded to conditions it encountered in live operation, conditions that emerged from real market dynamics rather than historical data selection. In practice, that distinction matters greatly to anyone evaluating a system for long-term capital relationship decisions.

Consistency Across Changing Market Regimes

One of the most important outputs of behavioural verification is regime consistency. Markets shift between different operating states. Trending environments, volatile regimes, and low-liquidity periods each create different conditions for a systematic trading engine to navigate. A well-designed system should maintain its structural behaviour across these shifts, even when its output frequency or capital deployment size changes.

For example, a system might reduce its frequency of deployment during a high-volatility regime. That reduction is not a failure. However, it must be verified as an intentional design output rather than an unintended response to system confusion or operational drift. Behavioural verification therefore means confirming that changes in output correspond to documented design logic rather than structural failure. That confirmation requires explicit regime-level analysis rather than aggregate performance review.

What Verified Behaviour Does Not Guarantee

Behavioural verification carries important limits that institutional observers should understand clearly. It does not guarantee future performance. It does not eliminate market risk. It does not confirm that the system will always find deployable opportunities. In addition, it does not prove that the system is optimal relative to alternative approaches.

What it does prove is structural consistency during the period reviewed. The system followed its documented rules. Its filtration logic operated as specified. Its permission layer responded correctly to changing conditions. For institutional observers, that proof provides a foundation for trust rather than a ceiling on scrutiny. It represents the minimum threshold for serious institutional consideration, not a final endorsement.

Regime Compatibility and Audit Standards in Systematic Trading

Audit standards in systematic trading must include explicit regime compatibility checks. These checks confirm whether the system’s permission layer responded correctly to different market environments. They verify that filtration logic tightened appropriately when data quality deteriorated. They also confirm that exposure constraints held when volatility exceeded normal operating parameters.

Regime compatibility review requires examining behaviour across multiple distinct market states, including periods when the system identified conditions as unfavourable and chose not to deploy capital. Structured inactivity is as important to verify as active deployment. A system that cannot demonstrate documented non-deployment during adverse regimes has not proven that its permission layer functions correctly. That verification gap is one of the core functions that audit standards exist to fill.

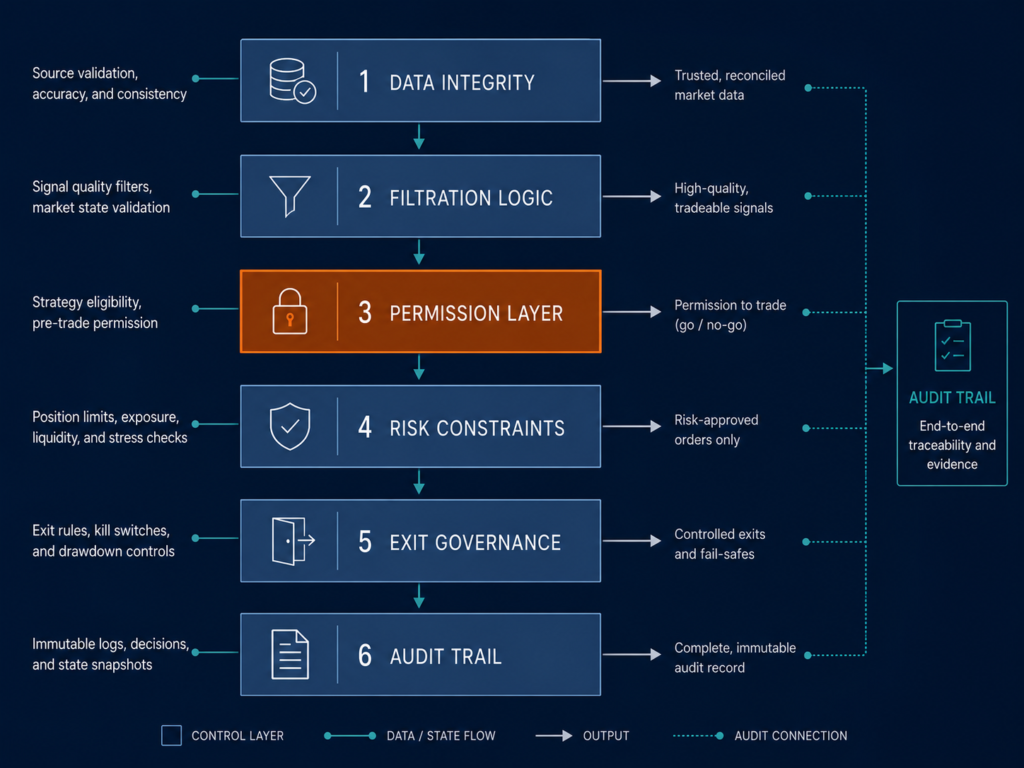

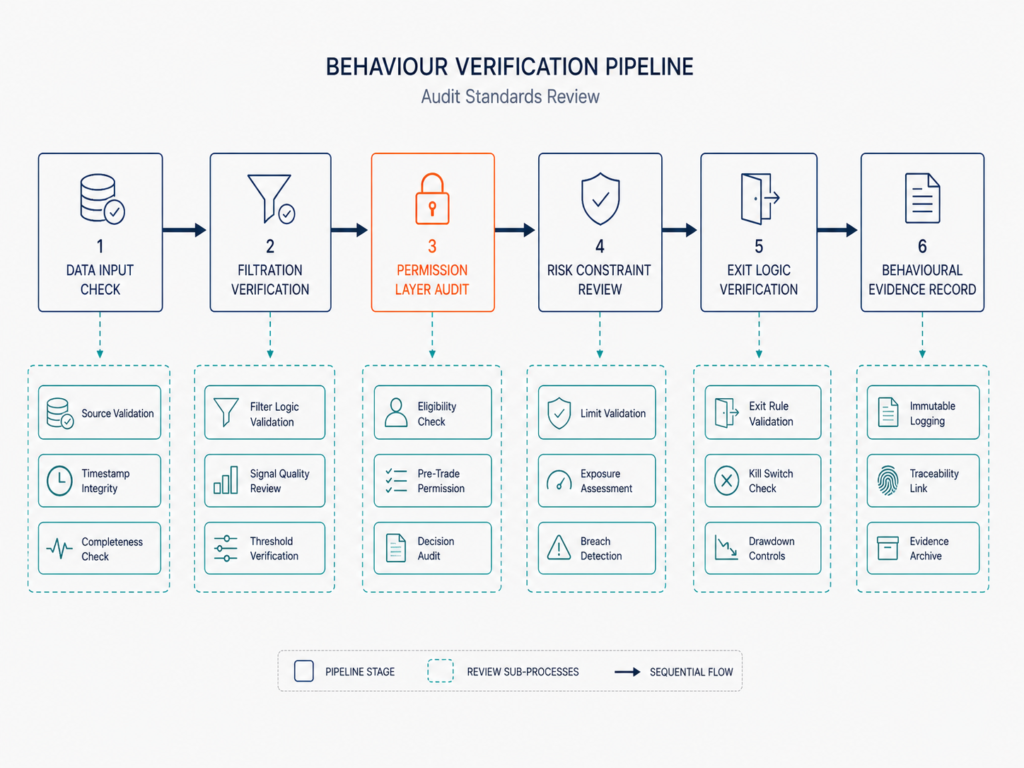

The Layers Audit Standards Systematic Trading Engines Must Address

Audit standards cannot operate effectively at the system level alone. They must penetrate each functional layer of the trading infrastructure, because failures occur at specific layers rather than across entire systems simultaneously. A review that examines only aggregate output will consistently miss layer-level failures that accumulate into systemic weakness over time.

The core layers that audit standards must cover include data integrity, filtration logic, risk constraints, permission architecture, and exit governance.

Data Integrity as the Foundation of Audit Standards

Data integrity sits at the base of every meaningful audit. Audit standards must confirm that the data inputs the system relied upon were clean, timely, and consistent with the system’s documented requirements throughout the review period.

A system that performed correctly on corrupted data has not demonstrated structural reliability. It has demonstrated coincidental alignment between flawed inputs and acceptable outputs. That coincidence will not persist under different data conditions. Therefore, data integrity review covers missing value handling, corporate action adjustments, pricing source consistency, and changes to the instrument universe. Furthermore, it covers whether the system applied its data trust rules correctly when input quality fell below acceptable thresholds. Without a documented data quality standard, audit standards have no benchmark for comparison on this layer.

Audit Standards Systematic Trading and Filtration Logic

Filtration logic is among the most operationally critical layers for audit standards in systematic trading to address. The filtration layer determines which instruments and market conditions advance to the permission and capital deployment layers. If filtration breaks down, every downstream decision operates on inputs it was not designed to handle.

Audit standards must verify that filtration behaved consistently throughout the review period. They must confirm that instruments excluded by filtration rules did not appear in the deployment layer. They must also confirm that new instruments entering the universe passed the required filtration checks before becoming eligible for capital allocation.

Filtration failures are particularly difficult to detect through performance review alone. A filtration breach may still result in a profitable trade. However, a profitable trade that bypassed filtration represents a structural failure regardless of its outcome. Audit standards surface that failure. Performance records do not.

Risk Constraint Verification and Audit Standards

Risk constraints form the protective boundary of any systematic trading engine, and audit standards must verify that those constraints held throughout the review period. Position sizes must have remained within documented limits. Exposure concentration must not have exceeded sector or instrument thresholds. The drawdown halt policy must have triggered correctly under the conditions that warranted it.

The principles behind well-designed drawdown and halt governance are foundational to this layer of verification, because the halt mechanism is one of the most structurally critical constraints an engine can implement. Risk constraint verification is particularly important during stress periods. A system that maintained its limits during calm market conditions has passed only a preliminary test. A system that held its constraints during a volatile or adverse regime has produced meaningful behavioural evidence that audit standards can confirm and document.

Exit Logic Within Audit Standards

Exit logic governs how a system closes positions and releases capital. Audit standards must verify that exit decisions followed the system’s documented rules rather than discretionary judgment applied in the moment. Time-based exits, risk-based exits, and target exits each require individual verification.

Exit logic failures often appear as extended holding periods beyond documented parameters or as positions closed using criteria the system was not designed to apply. Both represent behavioural drift. In practice, exit logic failures are among the hardest to detect through performance review, because they may not produce visible losses in the short term. Audit standards create the framework for identifying them before they compound into more significant structural divergence.

Audit Standards Systematic Trading How Differ From Backtesting

Backtesting and audit standards in systematic trading serve fundamentally different purposes. Backtesting applies a system’s documented logic to historical data to model expected behaviour under past conditions. Audit standards evaluate whether actual behaviour in live operation matched that documented logic. These are not equivalent exercises. Confusing them produces dangerous gaps in institutional review that performance monitoring alone cannot close.

Backtest Limitations and Audit Standards

Backtests carry several well-documented limitations that audit standards are specifically designed to address. Backtests operate on selected historical data and cannot include regimes the live system has not yet encountered. They also cannot model all execution frictions encountered in live markets, including slippage, fee drag, and order type constraints. Furthermore, most backtests do not account for operational errors or data quality issues that occur in live environments.

Audit standards address exactly these limitations. They evaluate the live system, including all execution friction, all operational variance, and all conditions the backtest did not anticipate. For that reason, institutional observers treat audit-verified behaviour in systematic trading as substantially more meaningful than backtest-verified logic. A strong backtest confirms a design principle. A strong audit confirms a live operating system.

Live Behaviour Verification and Stress Testing

Live behaviour verification examines how the system performed during conditions that were genuinely adverse or structurally different from its primary design environment. This includes elevated volatility periods, liquidity compression events, and market structure disruptions.

Stress period review is not optional within a rigorous audit framework. A system reviewed only during favourable conditions has not demonstrated behavioural resilience. Audit standards must therefore include deliberate examination of adverse periods rather than defaulting to aggregate performance across all conditions. A system that maintained its structural discipline during market stress has produced the strongest form of institutional evidence: verified behaviour under conditions that expose structural weaknesses in systems that are not robustly designed.

Building Audit Standards Into System Governance

The most reliable audit processes do not begin after a system goes live. They begin during system design. A system built with auditability as a foundational constraint produces structured evidence throughout its operation rather than requiring retrospective reconstruction when institutional review arrives.

This design-first approach to audit standards in systematic trading means treating governance documentation, change control, and behavioural logging as operational requirements rather than compliance obligations added at the end of the build process.

Documentation as Audit Standards Infrastructure

Documentation is the foundation that makes audit standards operational in any systematic trading context. Without clear documentation of rules, thresholds, and expected behaviours, verification has no standard to compare against. Reviewers cannot confirm compliance with undocumented constraints.

Effective documentation covers rule specifications, threshold values, regime definitions, permission conditions, exit criteria, and data quality requirements. Additionally, it covers any changes made to those parameters and the rationale for each change. Without this foundation, audit standards become impossible to apply with precision. In practice, systems that lack documentation cannot meaningfully pass an institutional audit. They can only report output, which is precisely what audit standards are designed to go beyond. System integrity depends on this documentation discipline as much as it depends on any technical constraint embedded in the engine itself.

Change Control and Audit Standards in Practice

Change control is a critical component of audit standards in systematic trading. Every modification to a rule, threshold, or parameter creates a potential break in the behavioural record. Without structured change control, reviewers cannot distinguish between intended design evolution and unintended system drift.

Effective change control logs every modification with a timestamp, a documented justification, and a record of the previous parameter value. It also records the review process that approved the change. Consequently, audit standards can isolate the behavioural impact of each change and evaluate whether post-change behaviour aligned with the documented intent of each modification. Systems that implement this discipline produce a continuous audit trail rather than requiring a retrospective reconstruction effort when institutional review is requested.

What Institutional Allocators Need From Governance

Institutional allocators approach systematic trading governance with a specific set of concerns. They want evidence that the system followed its own rules throughout the review period. They want confirmation that risk constraints held under pressure. They also want assurance that changes to the system followed a structured process rather than discretionary adjustment by individual operators.

Governance structures that satisfy these concerns require systematic documentation throughout the operating period, including records of decisions, changes, and the conditions under which the system chose not to act. Structured inactivity is as important to document as active deployment. A system that can show it declined to deploy capital during conditions its rules identified as unsuitable has demonstrated something performance records cannot show: that its permission layer was genuinely operational rather than theoretical.

What Audit Standards Prove to Institutional Observers

Audit standards in systematic trading ultimately serve a trust-building function. They provide institutional observers with structured evidence that extends beyond return records into the operating logic of the system itself. That evidence is durable in a way that performance figures are not, and it compounds across successive review cycles in a way that no single result period can replicate.

Behavioural Evidence as an Institutional Asset

Verified behavioural evidence represents one of the most durable assets a systematic trading operation can build. Performance records fluctuate with market conditions. Behavioural evidence, however, demonstrates structural discipline across a range of conditions, including adverse ones. That distinction matters greatly to allocators who evaluate systems over multi-year horizons rather than quarterly performance windows.

A system that demonstrates consistent rule adherence, stable filtration behaviour, intact risk constraints throughout stress periods, and structured change processes has built institutional credibility that performance records alone cannot replicate. Furthermore, that credibility compounds over time. Each audit cycle adds to the documented behavioural record, building a structural history that supports long-term capital relationship decisions with a quality of evidence that results-only reporting cannot produce.

Audit Standards Systematic Trading ad The Long-Term Role

Audit standards in systematic trading are not a compliance exercise. They are a design discipline that shapes how systems operate across their full lifecycle. Systems built with auditability in mind document their behaviour continuously. They produce evidence structures that support institutional review at any point in their operation. They also create internal feedback loops that identify behavioural drift before it compounds into structural failure.

This means treating audit standards not as an end-of-period review but as an ongoing operating discipline. The goal is not to pass a review. The goal is to build a system that produces auditable evidence as a natural output of its design, in the same way that a well-governed institution produces records not to satisfy auditors but because accurate documentation is foundational to sound operation.

Conclusion: Behaviour Is the Evidence

The institutional case for systematic trading ultimately rests on behaviour, not performance. Performance records answer what happened. Audit standards in systematic trading answer whether the system behaved as designed, held its constraints under pressure, and maintained structural integrity across changing market conditions.

Those answers matter more than return figures for institutional observers who make long-term capital decisions. Verified behaviour does not eliminate uncertainty. However, it transforms the quality of evidence available to allocators and institutional partners. A system with a clear audit trail, a consistent behavioural record, and structured governance produces a different kind of confidence than a system with strong returns and no documented process.

That confidence is what audit standards exist to produce. For trading infrastructure built to last, auditability is not an optional layer added after the fact. It is a foundational design requirement. Systems that treat it as such build evidence structures that support institutional relationships over time, while systems that do not remain permanently exposed to the question that performance records cannot answer: did the system truly behave as designed?

About the Author

Dovest develops systematic trading infrastructure focused on structure, constraints, and governance that make engine behaviour stable, explainable, and auditable under real-world stress. This article reflects institutional research and behavioural framework development.

Disclaimer: This article is provided for institutional research and educational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any financial product. References to systematic trading infrastructure and audit frameworks describe research and design principles and should not be read as performance claims or product availability statements.