Why Execution Layer Design in Systematic Trading Removes the Scalp vs Swing Binary

Most systematic trading frameworks force a choice before the trade begins. Scalp or swing. Short horizon or extended hold. Quick exit or patient position. This binary feels intuitive. However, it reflects a design constraint, not a market reality. Execution layer systematic trading removes that constraint entirely. Specifically, the decision shifts from “how long do I plan to hold” to “have entry conditions changed?”

That is a fundamentally different question. Furthermore, it produces fundamentally different system behaviour.

This article explains three things. First, why the scalp vs swing binary fails as system design. Second, how proper execution layer architecture resolves it. Third, what infrastructure must do to govern holding logic without imposing artificial time horizons.

Why the Scalp vs Swing Binary Fails as System Design

What the Binary Assumes About Markets

The scalp vs swing binary assumes traders set a time horizon before entry. In practice, markets do not cooperate with pre-set timelines. A mean reversion opportunity on a liquid equity may resolve in ninety minutes. However, the same setup may equally require five sessions before price returns to its expected range.

The asset does not know which outcome the trader preferred. Moreover, the system should not care. The system should ask one question only. Do the conditions that justified the original decision still hold structurally?

Execution layer systematic trading starts from this observation. As such, holding duration is not an input. Instead, it emerges from ongoing condition assessment, not from a pre-committed timeline.

How the Binary Creates Artificial Deadlines

When a trading system separates scalp logic from swing logic as two distinct modes, it introduces a deadline the market did not create. The scalp mode exits because the timer expires, not because price resolved. By contrast, the swing mode holds because the label says “swing,” not because conditions confirm continued validity.

Both decisions carry operational risk. Specifically, forced exits can realise losses at structurally weak moments. In addition, extended holds without condition review can expose capital to deteriorating risk profiles.

By contrast, execution layer systematic trading treats holding duration as a continuous governance question. The system monitors conditions after entry using the same framework it applied before entry. Therefore, exit logic follows from condition change, not from a pre-assigned mode.

Why Execution Layer Systematic Trading Breaks This Pattern

A properly designed execution layer separates four distinct decisions:

- Whether conditions support entry

- What risk the position carries at the moment of entry

- Whether conditions still support holding after each session

- When conditions confirm the original expected behaviour has resolved

Each of these is a distinct decision point. Additionally, each belongs to a distinct layer within the architecture. The execution layer governs the third and fourth decisions continuously. It does not inherit a time horizon from the entry signal. Instead, it inherits a risk definition and a condition set, and then monitors both.

For this reason, well-designed execution layer systematic trading does not ask “is this a scalp or a swing?” Instead, it asks “have exit conditions been met?” If no, the position continues. If yes, the position closes.

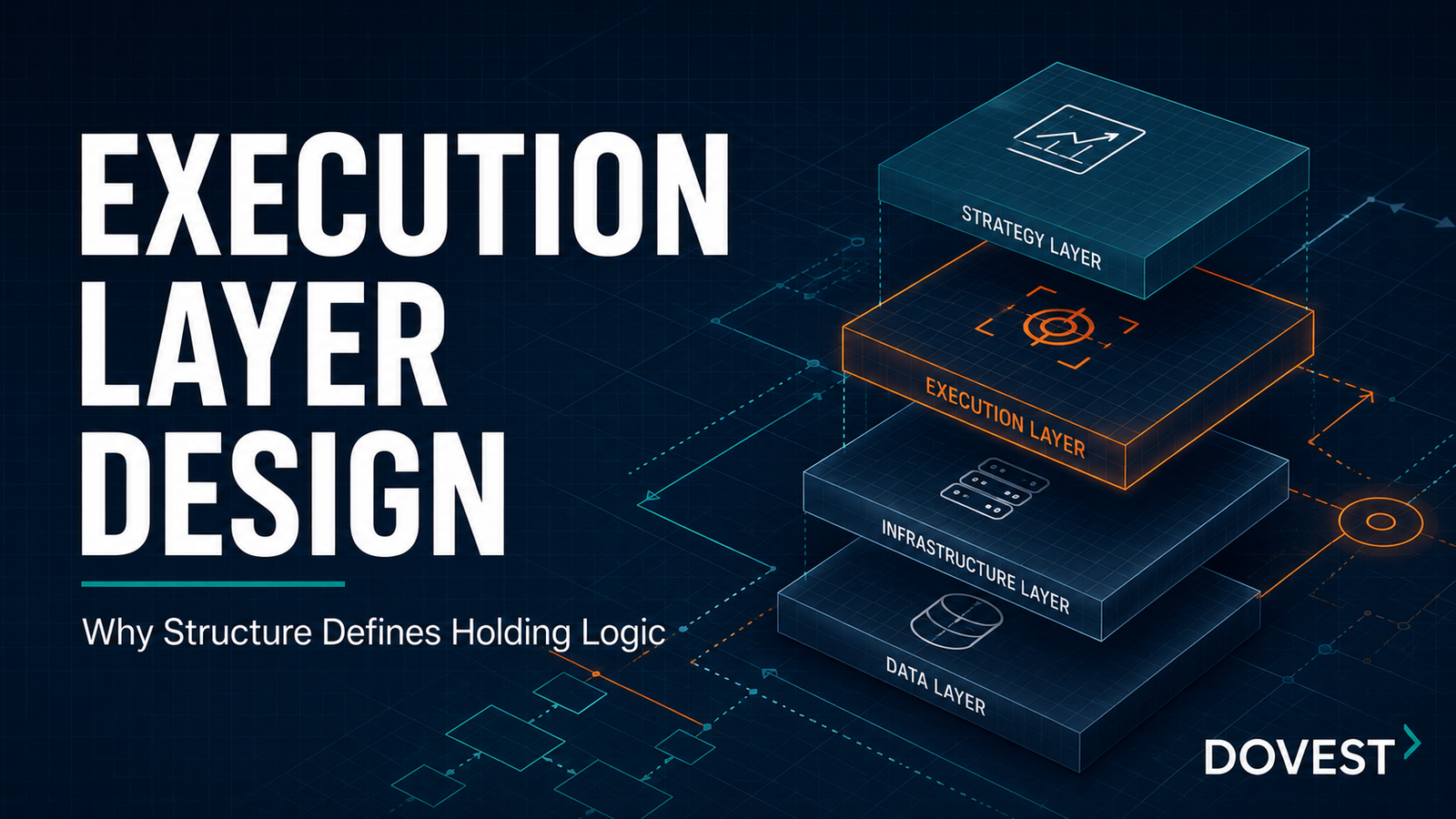

The Architecture Behind Execution Layer Design

Signal Layer and Execution Layer Must Remain Separate

One of the most common architectural failures conflates signal generation with execution governance. The signal layer identifies when conditions may support a trade. However, it does not determine how long capital stays exposed.

In execution layer systematic trading, these responsibilities stay explicitly separated. The signal layer communicates opportunity. By contrast, the execution layer governs capital exposure from entry through exit. Consequently, holding duration emerges from execution layer logic, not from any property of the original signal.

This separation creates a cleaner system. Equally, it creates a more honest one. The system does not claim a short-duration signal predicts a short-duration outcome. Instead, the architecture acknowledges that resolution timing is uncertain. As a result, governance manages that uncertainty without forcing arbitrary exits.

How the Permission Layer Governs Execution

Before the execution layer can act, the permission layer must confirm that conditions support capital deployment. In execution layer systematic trading, permission is not a binary switch. Instead, it narrows progressively as conditions deteriorate.

At entry, the permission layer checks four factors. Regime compatibility. Liquidity sufficiency. Volatility context. Structural quality. If all checks pass, capital receives permission to enter. Importantly, the execution layer then inherits this permission as a starting state, not as a permanent approval.

Throughout the holding period, the execution layer monitors whether the original permission conditions still apply. Furthermore, it checks whether new risk factors have emerged that would narrow or revoke permission. As such, ongoing permission assessment allows the system to hold positions appropriately without becoming blind to changing conditions.

For useful context, the filtration logic in systematic trading framework operates on similar principles. In particular, the filtration layer and the execution layer share the same structural logic. Conditions must remain valid for capital to remain exposed.

Risk Definition at Entry in Execution Layer Systematic Trading

Execution layer systematic trading requires complete risk definition at the moment of entry. Specifically, the trader must set position size, maximum acceptable loss, and exit triggers before the trade begins.

The practical effect of this rule is significant. The system does not adjust risk parameters in response to mark-to-market movement. Furthermore, it does not widen stops because a position is temporarily underwater. In addition, it does not reduce position size mid-trade because sentiment has shifted.

Instead, the execution layer enforces the risk definition established at entry. As a result, holding duration can extend without increasing risk exposure beyond the original design. The position holds because conditions remain valid, not because capital is chasing recovery from an oversized loss.

How Multi-Layer Execution Works in Practice

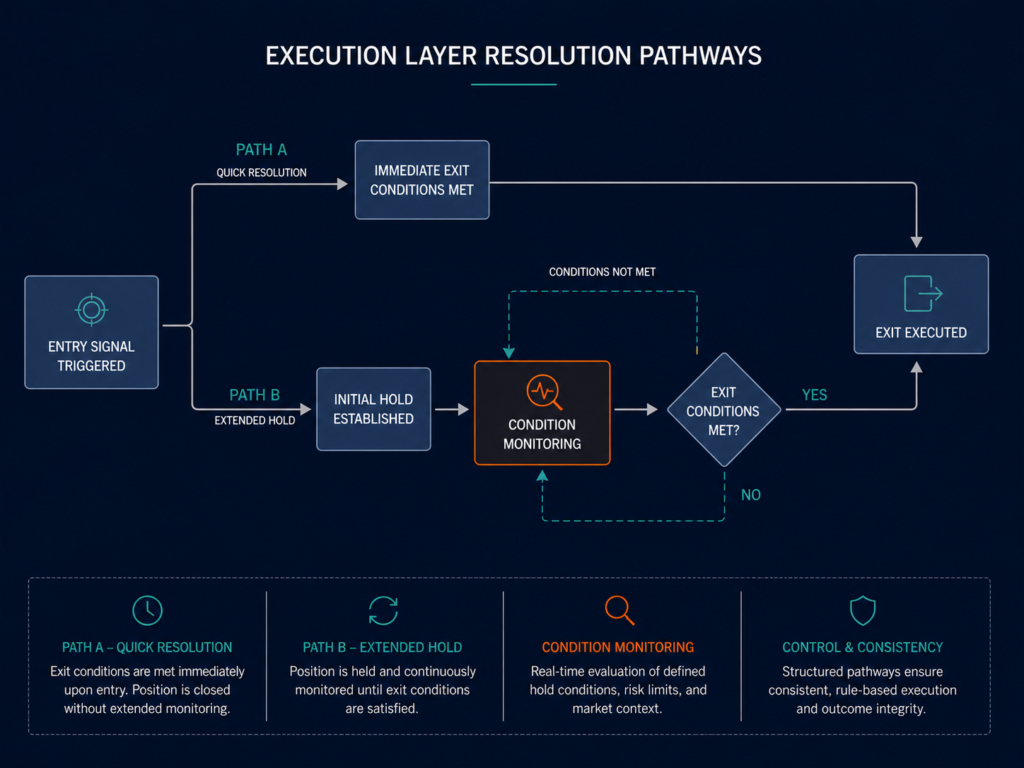

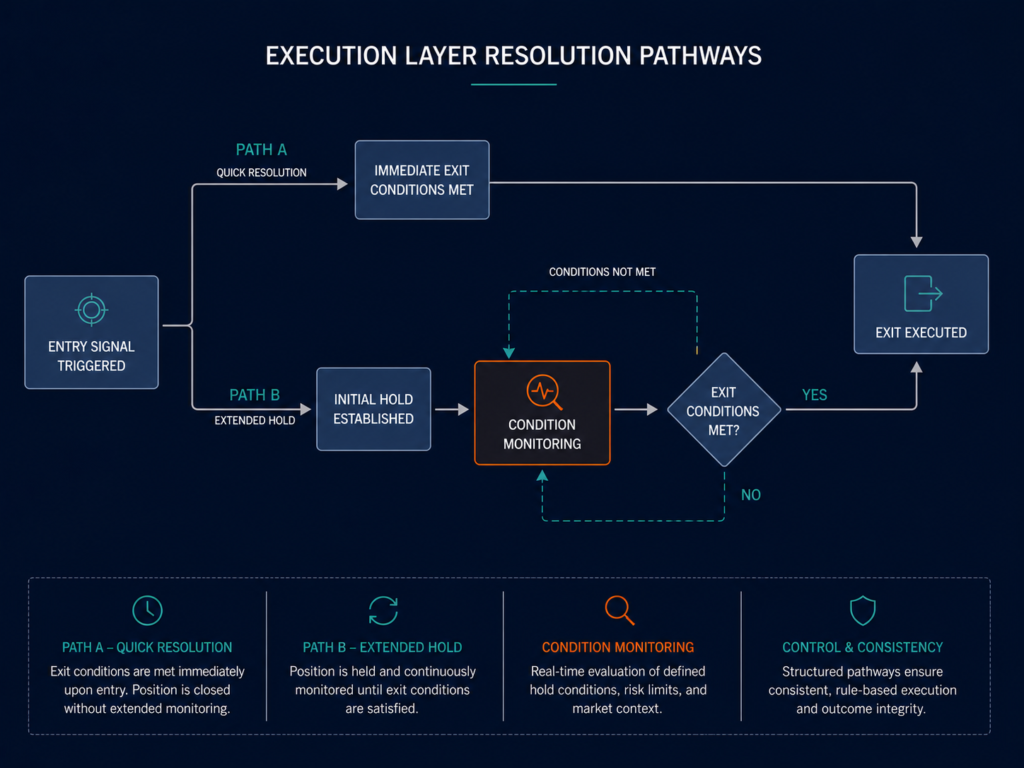

When the Short-Term Resolves Quickly

When mean reversion resolves quickly, the execution layer simply confirms the target exit condition has triggered and closes the position. The system then resets to its monitoring state. If conditions remain compatible with a new entry, the permission layer assesses the opportunity fresh.

This behaviour is not re-entry in the traditional sense. The system does not “try again” because the previous trade worked. Instead, it evaluates the current condition independently. Furthermore, it applies the same filtration and permission logic, then either confirms or denies the next position.

Therefore, the same instrument may appear in the signal log multiple times across consecutive sessions. This reflects correct system behaviour. In practice, each entry follows its own independent condition assessment.

When the Market Needs More Time

When mean reversion does not resolve within the expected window, the execution layer does not force an exit. However, it does not simply wait passively either. Instead, the execution layer continues monitoring the conditions that justified the original entry.

Specifically, it checks three things. First, whether regime compatibility has changed. Second, whether the structural basis for the trade remains intact. Third, whether the position has breached the risk floor set at entry. If conditions remain valid, the position continues to hold. By contrast, if conditions deteriorate, the exit logic activates regardless of whether the position is profitable.

This is a critical distinction in execution layer systematic trading. The exit decision does not depend on the P&L. Instead, it depends on whether the original structural thesis still holds.

As a result, positions can naturally extend across multiple sessions without requiring a conscious decision to “switch to swing mode.” In practice, the extension reflects ongoing condition validity, not a deliberate strategy change.

Execution Layer Systematic Trading and Mean Reversion Dynamics

Mean reversion strategies depend on a specific thesis. Short-term dislocations in structurally sound instruments resolve toward their expected range over time. However, “over time” is inherently uncertain. In some cases, resolution takes hours. In other cases, it takes days.

A system that forces time-horizon selection before entry essentially bets on which resolution window the market will use. By contrast, execution layer systematic trading avoids this bet. Specifically, the framework defines structural conditions for resolution and monitors whether conditions still hold, regardless of how many sessions that takes.

This approach aligns naturally with how mean reversion dynamics actually behave in liquid equity markets. Price does not resolve because a timer expires. Instead, it resolves when buying and selling pressure reach a point where the dislocation closes. As such, the execution layer monitors for that point, not for a calendar date.

What Holding Logic Actually Does Inside the Execution Layer

The Role of Exit Conditions in Systematic Trading

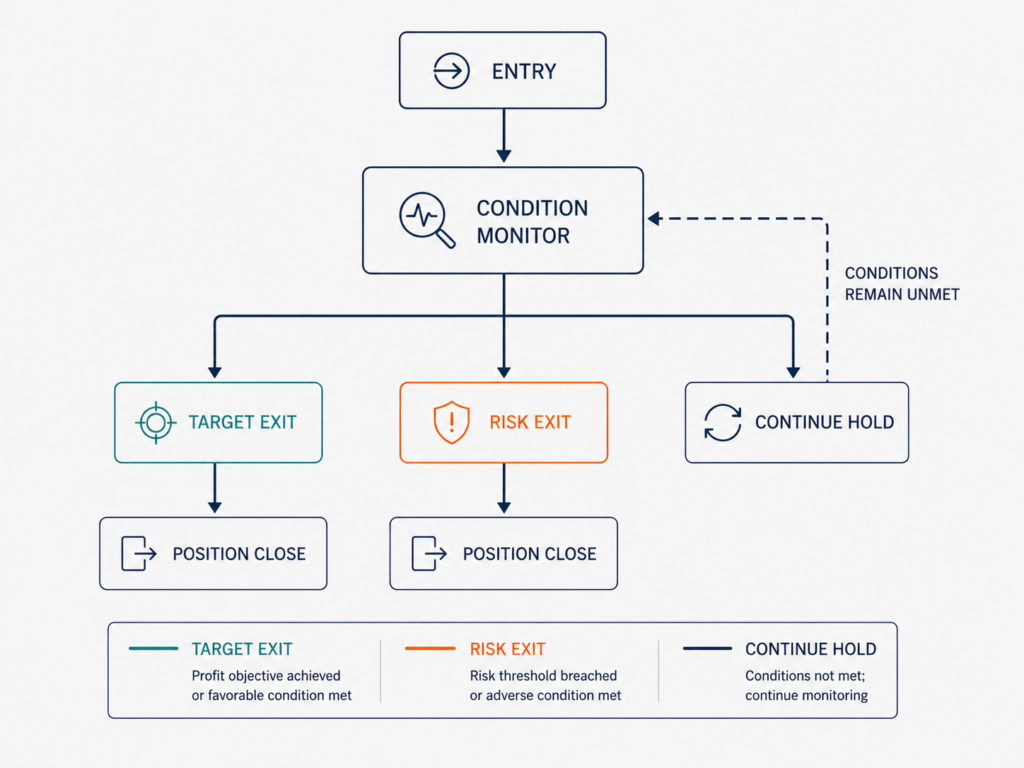

Exit conditions in a well-designed execution layer fall into three categories. Target exit conditions confirm the expected mean reversion behaviour has completed. Risk exit conditions confirm the position has reached the original risk floor, regardless of thesis. Time-based review conditions trigger condition re-assessment after a defined period without resolution.

Each operates independently within the execution layer. Furthermore, each takes precedence in a defined order. Risk exits always activate regardless of thesis status or time elapsed. Target exits activate when resolution confirms. By contrast, time-based reviews trigger re-assessment rather than automatic exit.

This hierarchy keeps holding logic structured and auditable. In practice, the execution layer can hold a position for an extended period without ever losing sight of its original risk definition.

How the Execution Layer Avoids Forced Exit

Forced exits carry a specific operational risk. Specifically, they can realise losses at structurally weak moments simply because a pre-set timer expired. In execution layer systematic trading, forced exits trigger only when risk conditions activate, not when time conditions activate.

This design choice reflects a clear priority. Protecting the risk floor matters more than conforming to a pre-defined time horizon. A position that stays within its original risk parameters and continues to reflect valid structural conditions has no operational reason to close.

Pre-commitment rules, as covered in pre-commitment rules and decisions made before pain, establish the governance framework that makes this possible. By design, the execution layer enforces rules set before entry. Therefore, it does not respond to emotional pressure during the hold.

Capital Efficiency Through Execution Layer Design

A common objection to extended holding is that capital becomes idle. In execution layer systematic trading, position sizing addresses this concern, not forced exits.

Because the system defines risk completely at entry, the capital committed to each position reflects the maximum acceptable exposure. The architecture does not oversize positions in anticipation of quick exits. Consequently, capital remains appropriately allocated whether the position resolves in one session or five.

Moreover, the instrument universe in a multi-layer execution system is typically wide enough to generate new opportunities while existing positions are still open. As such, capital does not need to cycle through forced exits to remain active. Instead, position sizing governs how much capital each open position consumes, and the remaining capacity funds new entries when conditions support them.

Why This Matters for Systematic Trading Infrastructure

Execution Layer Systematic Trading vs Signal-Led Approaches

Signal-led systems define exit logic as a property of the signal itself. A short-duration signal produces a short-duration hold. By contrast, an extended signal produces an extended hold. The signal type encodes the time horizon directly.

By contrast, execution layer systematic trading defines exit logic as a property of condition monitoring. The signal identifies the opportunity. The execution layer governs exposure independently of what the signal predicted about timing.

In practice, this distinction produces more stable system behaviour under varying market conditions. When the market environment changes, a signal-led system must update its signal library to match. By contrast, an execution layer architecture simply continues monitoring conditions, because its logic applies regardless of regime.

This architectural choice also matters for scaling across markets. The same execution layer logic can support an ASX deployment today and extend to US S&P 500 instruments tomorrow. Specifically, only the data interface changes. The holding logic, the permission layer, and the risk definition all remain identical. As such, execution layer systematic trading scales by market interface, not by rule rewrite.

Monitoring the Execution Layer Under Real Conditions

Execution layer systematic trading requires active monitoring infrastructure. Specifically, the execution layer must communicate its state clearly. Which positions are open. What conditions currently apply. What exit thresholds are active. Whether any conditions have changed since entry.

This monitoring obligation is not optional. As such, it forms part of what makes the execution layer trustworthy as an infrastructure component. A holding position no one can audit is not a disciplined position. Instead, it represents an open risk with no clear governance.

Therefore, execution layer design must include logging, state visibility, and review cadence. In practice, these governance requirements apply regardless of how many sessions a position has been open.

The Governance Dimension of Execution Layer Design

Execution layer systematic trading creates an auditable record of every holding decision. Each session during a hold produces a condition assessment. That assessment either confirms continued validity or triggers an exit review. As such, the log of these assessments provides evidence the hold was governed, not simply forgotten.

This auditability matters particularly for institutional infrastructure. Allocators and risk teams need to understand not just what the system did. Furthermore, they need to understand why the system held a position across multiple sessions. The execution layer governance record answers that question directly.

In addition, this record supports post-trade analysis. When a position eventually closes, the system can review whether the holding logic performed as designed. If conditions changed faster than the monitoring cadence captured, that signals a system design issue, not simply an operational loss.

Execution Layer Design as Infrastructure, Not Feature

The scalp vs swing binary persists in trading system design because it is simple to implement and easy to explain. However, simplicity that conflicts with market reality produces fragile systems. When markets do not cooperate with pre-set time horizons, the system either forces a bad exit or ignores its own rules.

Execution layer systematic trading resolves this challenge. Specifically, the architecture treats holding duration as an emergent property of condition monitoring. As such, the framework governs exposure continuously rather than committing to a timeline. The system defines risk at entry and enforces it throughout. Furthermore, exit logic follows from condition change, not from a calendar.

This is not a feature added to an existing signal system. Instead, it is a foundational architectural choice. By design, this choice determines how capital behaves from the moment of entry to the moment of close. In particular, it determines whether the system stays governed under extended holds, or simply becomes a position no one knows how to manage.

Building this layer correctly requires clarity about what the execution layer is responsible for and what it is not. Signal detection is not its job. Permission assessment is not its primary function. Instead, its job is clear. Govern exposure from entry through exit, with full awareness of the risk definition set at entry and the conditions required for exit.

That is what systematic trading infrastructure does when engineers build it to handle market reality rather than theoretical assumptions about time horizons.

Continue learning about systematic behaviour frameworks.

For related research, explore how system integrity in trading governs architecture decisions from signal through exit.

Author

This article reflects the system design philosophy behind Dovest, an institutional systematic trading infrastructure company based in Australia. Dovest focuses on building and monitoring systematic engines where behaviour remains stable, explainable, and auditable under real-world stress. Content reflects research and framework principles only. It does not constitute financial advice.

Disclaimer

Dovest content serves institutional research and educational purposes only. It does not constitute financial advice, investment advice, trading signals, or a recommendation to buy or sell any financial product. References to systematic trading infrastructure describe research and design principles. As such, readers should not interpret these as performance claims or product availability statements.