Why Auction Behaviour Makes Trend Days Feel Different

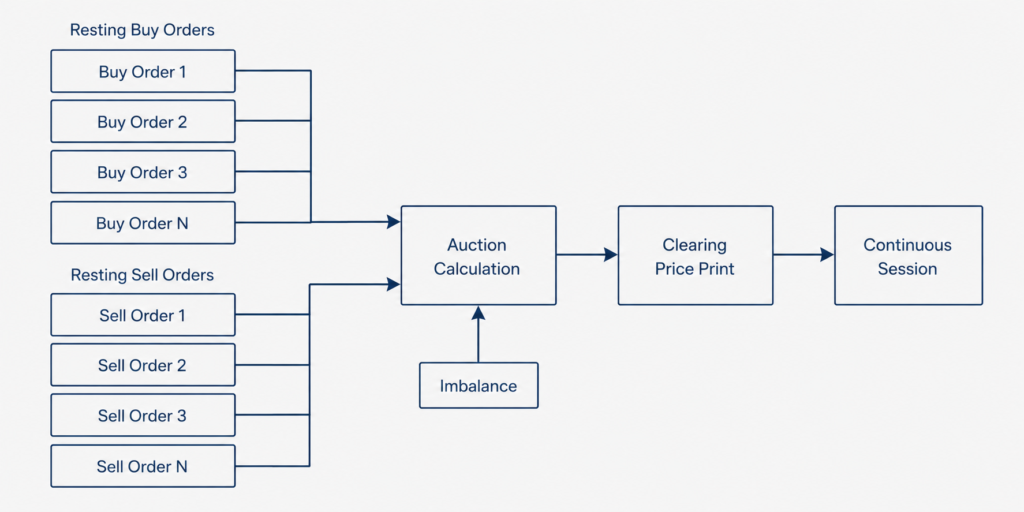

Auction behaviour describes how a market sets price when continuous trading pauses and orders concentrate into a single clearing event. Every trading session opens and closes with an auction. Furthermore, many venues run intraday auctions when volatility moves beyond a defined band. Each of these moments compresses supply and demand into one print. As a result, they expose the structural character of a session far more clearly than any single continuous tick. On trend days, that character changes in a visible way. The auction widens, imbalance persists, and the close confirms direction. Therefore, reading auction behaviour gives systematic infrastructure a structural lens that continuous price alone cannot offer.

Most retail frameworks treat the open and the close as routine timestamps. By contrast, systematic infrastructure treats them as concentrated information events. The auction is where conviction shows itself. Specifically, it reveals whether participants will commit size at a single agreed price. A thin, balanced auction signals indecision. A wide, one-sided auction signals pressure. In this way, the auction works as a structural summary of the whole session.

This article examines auction behaviour as a market structure property. In particular, it covers what auctions reveal, why trend days reshape them, and how disciplined engines turn that read into rules. The approach stays behaviour-first throughout. Structure comes first, and prediction never enters the design.

What Auction Behaviour Reveals About a Trading Session

An auction is a clearing mechanism, not a formality. It collects buy and sell interest across a short, defined window. Then it prints the single price that maximises executable volume. Consequently, the auction print carries more structural weight than any individual continuous trade. It represents agreement among many participants at one moment. For a systematic engine, that property makes the auction a reliable reference point rather than a passing quote.

Auction behaviour as price discovery, not noise

Many traders dismiss the open and the close as mechanical events. However, the auction is the purest price discovery moment of the session. It forces every resting order into one shared calculation. Therefore, the resulting price reflects genuine willingness to transact.

Auction behaviour, observed across many sessions, becomes a stable structural signal. For systematic engines, that stability is the whole point. A signal that holds across regimes can support a durable rule. By contrast, a signal that flickers from day to day cannot. As such, the engine values the auction precisely because it resists noise that continuous ticks carry.

Consider a session where the opening auction prints with steady, one-sided demand. The continuous session then tends to carry that demand forward. In this case, the auction did not merely open the day. Instead, it described the day before it unfolded. That descriptive quality is exactly why the engine treats auction behaviour as a primary input.

Auction behaviour versus continuous price

Continuous price updates constantly, and it reacts to every small order. The auction does the opposite. It waits, collects, and then resolves. Moreover, the auction removes much of the micro-noise that distorts a single tick.

This difference matters for engineering. A behaviour-first system needs inputs that stay consistent under stress. Auction behaviour provides exactly that. In practice, the engine uses the auction as an anchor and the continuous session as confirmation. The two read together, never one alone.

This pairing also keeps the engine honest. A continuous tick can tempt a system into reacting fast. The auction, by contrast, slows the read down to a structural pace. Therefore, the engine gains speed where it helps and patience where it matters most.

The structural role of the auction

The auction sits at the boundary between two market states. Before it, orders rest without execution. After it, continuous trading resumes. As such, the auction marks a clean transition in market structure.

It also tells an engine how a session begins and how it settles. Moreover, the distance between the opening auction and the prior close measures overnight repricing directly. In practice, that gap is one of the cleanest structural inputs a behaviour-first system can use. The engine does not interpret it emotionally. Instead, it logs the gap as a number and compares it against pre-set structural thresholds.

The transition also carries timing information. A session that opens far from the prior close has already moved before the engine acts. As such, the engine accounts for that displacement when it sizes any position. Structure and timing travel together in this read.

Why Trend Days Feel Structurally Different

Trend days are sessions where price moves persistently in one direction with shallow pullbacks. They feel different to a discretionary trader. More importantly, they look different at the structural level. The auction is where that difference first appears, often before the continuous session makes it obvious. Therefore, an engine that reads auctions well can recognise the regime early.

How trend days reshape auction behaviour

On a trend day, auction behaviour shifts in a recognisable pattern. The opening auction often prints with a large imbalance between buyers and sellers. That imbalance does not clear within the first few minutes. Instead, it persists well into the continuous session.

Furthermore, the closing auction on a trend day tends to extend the move rather than fade it. By contrast, a balanced day shows imbalance that resolves quickly and quietly. Therefore, the persistence of imbalance, not its initial size alone, is the real signal of a trend regime. A disciplined engine measures that persistence directly and treats it as structured evidence.

Persistence is measurable in a simple way. The engine tracks how long the opening imbalance survives into continuous trading. A short survival points to a balanced day. A long survival points to a trend. Consequently, the engine classifies the regime from duration, not from a single snapshot.

Range days and quieter sessions

Range days produce a very different signature. The opening auction clears close to the prior session’s close. Imbalance stays small, and it resolves fast. Additionally, the closing auction prints inside the day’s range rather than at an extreme.

In this way, the auction itself tells an engine which regime it is operating in. The engine does not need to forecast the regime in advance. Instead, it only needs to read the structure the auction has already revealed. Consequently, regime classification becomes an observation rather than a prediction. That distinction sits at the heart of behaviour-first design.

Range days also reward restraint. The structure offers fewer clean opportunities, and the engine recognises that early. Therefore, it commits less capital and accepts fewer trades. In this way, the auction protects the system from forcing activity into a quiet session.

Reading the Opening Auction

The opening auction sets the tone for the session. It absorbs overnight news, offshore index moves, and accumulated orders from the prior close. For this reason, it serves as the first structural checkpoint an engine examines each day. A clear read here shapes every decision that follows.

Opening auction imbalance and conviction

Imbalance is the core variable in the opening auction. It measures the size difference between buy and sell interest at the indicative clearing price. A large, stable imbalance shows that one side will pay up to transact. Consequently, the engine reads conviction in that structure.

A small or shifting imbalance shows the opposite. It signals hesitation among participants. In that case, the engine reads indecision and stays patient. Specifically, it withholds capital until the continuous session provides a clearer structural picture. Patience here is a rule, not a mood.

The engine also tracks how imbalance moves during the pre-open window. A build that grows steadily confirms genuine pressure. A build that swings back and forth warns of thin, unstable interest. As a result, the quality of the imbalance matters as much as its size.

What the opening print signals

The opening print also matters relative to the prior close. A wide gap that holds through the first hour suggests genuine repricing. By contrast, a wide gap that fills quickly suggests an overreaction the market is already correcting.

Therefore, the engine treats the opening auction as a hypothesis rather than a conclusion. It waits for confirmation. In practice, the continuous session either validates the structure the auction proposed or rejects it. As such, the engine acts only after that structural confirmation arrives, never before.

This patience has a cost, and the engine accepts it. Waiting for confirmation means the engine misses the very first move. However, it also avoids acting on a structure that never holds. For a behaviour-first system, that trade is always worth making.

The Closing Auction as a Session Signal

If the open sets the tone, the close delivers the verdict. The closing auction concentrates end-of-day rebalancing, index flow, and position adjustment into one print. As such, it carries unusually high information density. A behaviour-first engine therefore studies the close with particular care.

Closing auction behaviour and continuation

On trend days, closing auction behaviour tends to confirm the move. Price prints at or near the session extreme. Large participants add exposure rather than reduce it. Moreover, the close-to-close change aligns cleanly with the intraday direction.

This continuation pattern is one of the clearest structural markers of a genuine trend. Therefore, a behaviour-first engine weights the closing auction heavily when it classifies the session. In this way, the close becomes the deciding piece of structural evidence, not an afterthought tacked on at the end of the day.

The closing auction also carries forward into the next session. A strong, confirming close shapes how the engine reads the following open. Therefore, the close is not just a verdict on today. Instead, it also frames tomorrow’s first structural checkpoint.

Reading reversal risk at the close

Not every strong session closes strong. Sometimes the closing auction fades the move instead. Price pulls back toward the day’s mean, and the imbalance reverses direction.

In that situation, the engine reads exhaustion rather than continuation. Consequently, it adjusts how it carries risk into the next session. The close, read this way, becomes an early warning signal rather than a simple summary. This structural reading connects directly to broader market structure analysis in systematic trading, where session-level signals feed longer-horizon decisions across the engine.

A fading close does not trigger panic in a disciplined system. Instead, it triggers a documented adjustment. The engine reduces carried risk and waits for the next auction to clarify direction. In this way, reversal risk becomes a managed input rather than a surprise.

Intraday Auctions and Volatility Pauses

Continuous trading is not always continuous. When price moves too far too fast, many venues trigger a short auction. These volatility pauses are structural events in their own right. An engine that ignores them loses part of the session’s structural record. Therefore, a disciplined system treats every pause as data.

Volatility auctions as circuit logic

A volatility auction halts continuous matching for a brief, clearly defined window. It lets the order book rebuild before trading resumes. By design, the mechanism slows a disorderly move and restores orderly price formation.

For an engine, the trigger itself is information. It marks a precise moment where structure broke down and had to reset. Therefore, the engine records each trigger rather than treating it as a simple interruption. Each pause becomes a timestamped structural marker.

The engine also studies what happens immediately after a pause. A clean resumption suggests the reset worked. A second pause shortly after suggests deeper instability. Consequently, the sequence of pauses matters more than any single one in isolation.

Pre-open indicative auction behaviour

Before the opening print, most venues publish an indicative price and indicative imbalance. This pre-open phase is a live preview of auction behaviour as it forms. The numbers update as orders arrive and cancel.

A behaviour-first engine watches this phase closely. However, it does not act on it directly. Instead, it tracks how the indicative imbalance evolves toward the open. A steady, one-sided build signals conviction. A jumpy, reversing build signals noise. As such, the pre-open window becomes a structural warm-up read.

This phase also protects against surprise. By the time the auction prints, the engine already holds a structural expectation. Therefore, the actual print confirms or contradicts a view the engine formed minutes earlier. Surprise, in a well-built system, should stay rare.

Why intraday pauses inform auction behaviour

Each volatility pause adds to the session’s auction behaviour record. A day with several pauses is structurally fragile. A day with none is structurally calm. Therefore, the engine reads the count of pauses as direct regime evidence.

In practice, repeated pauses lower the size an engine is willing to commit. The logic is structural, not emotional. A fragile session offers a less reliable execution surface. As a result, the engine scales down until the structure stabilises again.

Over time, the pause record builds a structural profile of each instrument. Some names pause often and reward caution. Others rarely pause and support steadier sizing. As such, the engine learns instrument behaviour from the pause history itself.

How Systematic Engines Encode Auction Behaviour

Reading auctions is only useful when the read becomes a rule. Systematic infrastructure turns auction behaviour into explicit, testable inputs. It does not rely on interpretation in the heat of the moment. Instead, the engine defines its responses long before the session opens.

Encoding auction behaviour into entry rules

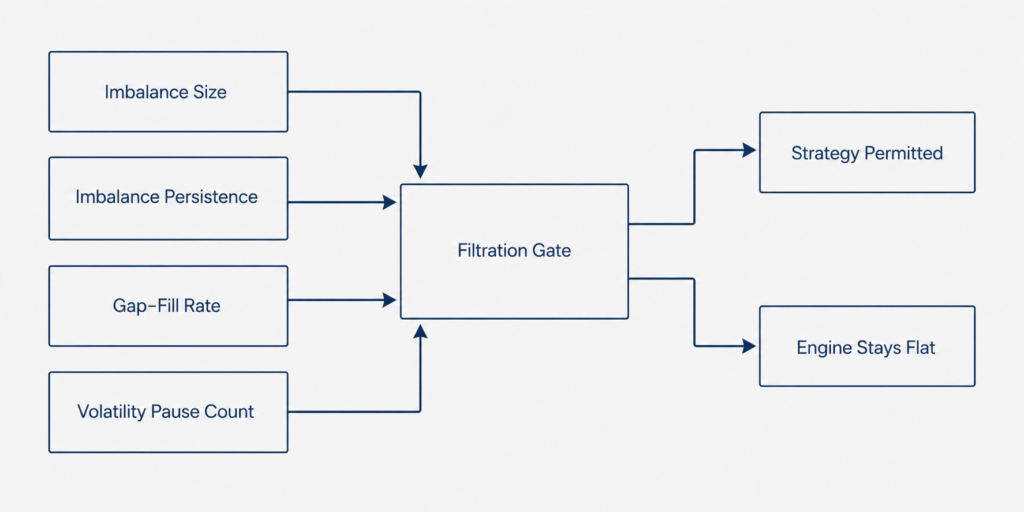

An engine encodes auction behaviour as a set of measurable variables. Imbalance size, imbalance persistence, gap-fill rate, and closing continuation all become numbers. The engine then defines thresholds for each variable in advance.

As a result, the engine makes its decision before the session starts, not under live pressure. The auction supplies the data. The pre-committed rule supplies the response. In this way, discipline becomes structural rather than personal. The engine never improvises a new threshold mid-session.

Encoding also makes the system testable. Every threshold can face historical sessions before it goes live. Therefore, the engine knows roughly how a rule behaves before it ever commits capital. Testability, not intuition, is what earns a rule its place.

Auction behaviour as a filtration input

Auction behaviour rarely acts alone inside a well-built system. Instead, it feeds a wider filtration layer alongside volatility regime and liquidity depth. The filter asks one structural question. Does the session’s auction signature permit the strategy to operate at all.

If the answer is no, the engine simply stays flat. If the answer is yes, the strategy proceeds within its defined limits. In this way, the auction becomes a gate rather than a trigger. The distinction matters, because a gate protects capital while a trigger merely spends it.

Filtration also keeps the engine consistent across regimes. The same gate runs on a calm day and a violent one. Only the inputs change, not the logic. As a result, the engine behaves the same way under stress as it does in quiet conditions.

Auction Behaviour Across ASX and US Venues

Auctions are not identical across markets. Each venue runs its own mechanism, timing, and participant mix. Therefore, an engine built for one market cannot assume the same auction signature in another. The structure must be re-measured for every venue before any rule applies.

ASX auction behaviour profile

On the ASX, opening and closing auctions concentrate a large share of daily volume into two windows. Index and fund flow in particular crowd into the closing print. As a result, ASX auction behaviour tends to be highly informative, yet very venue-specific.

An engine reading the ASX close must account for that concentration directly. Otherwise, it will misread routine structural flow as a directional signal. For this reason, venue calibration comes before strategy logic, never after. Moreover, the engine treats the ASX auction window as a fixed structural feature of the session, one it measures every day rather than assumes.

US auction behaviour profile

US large-cap venues operate across a deeper and more fragmented landscape. Order flow spreads across multiple venues both before and after the auction. Consequently, US auction behaviour carries a different texture from the ASX equivalent.

The same mean reversion logic still applies without change. However, the engine reads the structure through a new data interface, not a new strategy. This is why the algorithm stays market-agnostic by design. Differences in venue structure connect closely to documented microstructure variance across regions, which shapes how each market must be read.

Fragmentation also changes how the engine validates a US auction print. It cross-checks the print against flow on related venues. A consistent picture confirms structure. A divergent picture calls for caution. As a result, the US read demands more validation than the ASX equivalent.

Auction Behaviour in Risk and Execution Design

The final use of auction behaviour is risk. A structural read only has value when it changes how an engine sizes and exits. Discipline lives in that link. Without it, the read stays an observation with no consequence for capital.

Auction behaviour and position sizing

Auction behaviour informs how much capital an engine commits to a session. A clean, one-sided auction with persistent imbalance can justify a fuller allocation. A noisy, pause-heavy session calls for clear restraint instead.

Therefore, sizing follows structure rather than enthusiasm. The engine scales up on behaviour, never on the hope of a larger move. In this way, position size becomes a direct expression of the structural read, not a separate guess layered on top.

Sizing on structure also removes a common failure mode. A discretionary trader often sizes up after a good run. The engine does the opposite when structure does not support it. As such, the auction read keeps position size anchored to evidence rather than recent results.

The limits of auction behaviour as a read

Auction behaviour is a structural input, not a forecast. It describes the session in front of the engine. It does not predict the next one. Furthermore, auctions can mislead when news breaks mid-session or when liquidity thins without warning.

For this reason, a disciplined system treats the auction as one input among several. It never lets a single read override the wider risk framework. Instead, the auction earns its place by staying consistent, measurable, and explainable. Those three properties, rather than predictive power, are what make it genuinely useful.

A mature system also reviews its auction read after the fact. It compares what the auction implied against what the session delivered. Over many sessions, that review sharpens the thresholds. In this way, the limits of the read become the starting point for improving it.

Trend days feel different because their structure genuinely is different. The auction is where that structure first becomes visible to a disciplined observer. By reading the open, the close, and every volatility pause as concentrated information, a systematic engine can classify a session without ever predicting it. In this way, auction behaviour supports the core Dovest principle. Structure comes first, and prediction never enters the design.

Continue Exploring Dovest Research

Explore more behavioural research from Dovest. The series builds a structure-first view of systematic trading, one framework at a time.

About the Author

This article reflects the research perspective of the Dovest team. Dovest designs systematic trading infrastructure with a behaviour-first philosophy. The focus stays on structure, filtration, and risk architecture that keep engine behaviour stable, explainable, and consistent across markets. Dovest writes from an engineering standpoint, not a forecasting one. Every framework here describes how disciplined systems reason, rather than what any market will do next.

Disclaimer

This article is for educational and informational purposes only. It does not constitute financial, investment, or trading advice. Dovest does not provide signals, forecasts, or guaranteed outcomes. Readers should not treat anything here as a recommendation to buy or sell any security. Furthermore, readers should consult a licensed professional before making any financial decision.