Most trading frameworks treat volatility as a single number—a magnitude to be measured and managed. This approach overlooks a fundamental truth: volatility personality determines whether execution conditions remain structurally sound or silently deteriorate. Understanding volatility personality is not a modeling preference. For systematic trading infrastructure, it represents an upstream necessity that shapes every downstream decision: whether execution is permitted, how risk boundaries adapt, and when strategic inactivity becomes the disciplined response.

Why Volatility Magnitude Tells an Incomplete Story

Retail frameworks typically categorize volatility by size. High volatility signals danger. Low volatility suggests safety. This binary framing collapses under institutional scrutiny.

Two markets can exhibit identical volatility levels while behaving in fundamentally different ways. One absorbs shocks cleanly, normalizes quickly, and maintains execution integrity. The other fragments, persists through instability, and silently degrades the assumptions underlying position management.

Systematic trading infrastructure must distinguish between volatility magnitude and volatility personality. Magnitude answers “how much?” Personality answers the questions that magnitude cannot:

- Does volatility expand symmetrically across upside and downside movements, or does asymmetry dominate?

- Do shocks decay within predictable bounds, or do they persist and self-reinforce?

- Does the system recover smoothly, or do cascading effects emerge?

- Does volatility respect historical regime boundaries, or do structural breaks appear?

These behavioral characteristics determine whether execution remains valid at the infrastructure level.

Volatility Personality as an Execution Prerequisite

Most strategies carry implicit assumptions about volatility behavior, whether acknowledged or not. Mean reversion logic assumes fast decay and symmetric behavior. Momentum frameworks depend on directional persistence. Breakout strategies require clean expansion followed by stabilization.

When volatility personality shifts, strategies do not gradually weaken. They invalidate abruptly. Execution assumptions that held under one behavioral regime collapse under another.

This is why behavior-first systems evaluate volatility personality before any signal logic operates. Execution is not conditioned on forecast confidence. It is conditioned on behavioral compatibility—the structural alignment between market conditions and the assumptions embedded in execution logic.

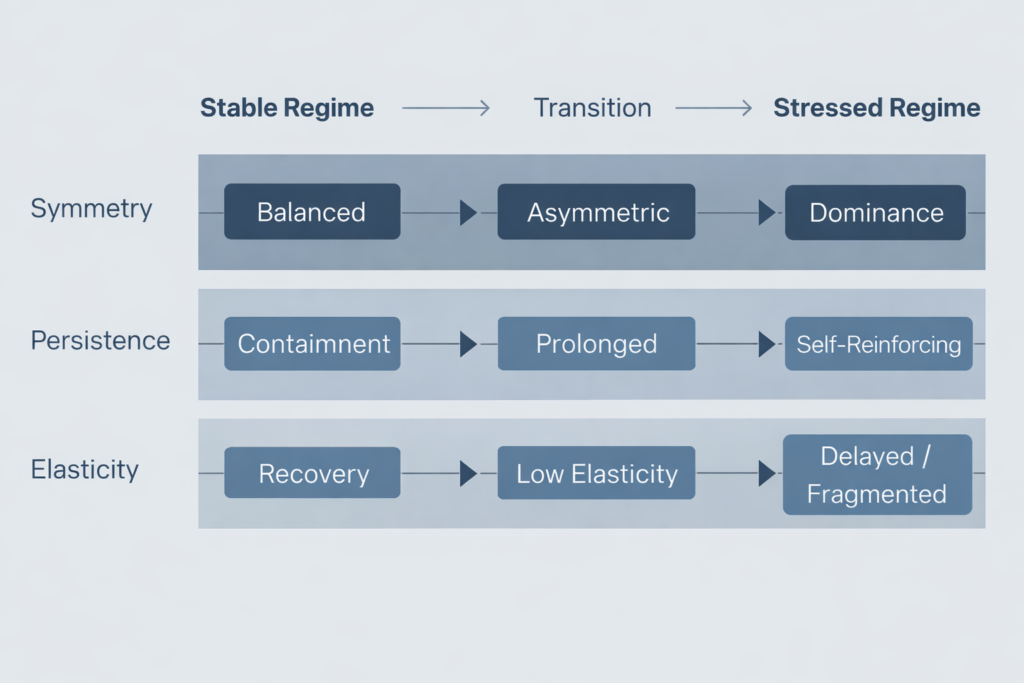

The Core Dimensions of Volatility Personality

Volatility personality becomes observable through a focused set of structural dimensions. These dimensions do not predict future price movements. They classify whether current market behavior supports execution integrity.

Understanding Symmetry vs Asymmetry in Volatility Personality

In stable regimes, volatility expansion tends to remain statistically balanced between upside and downside movements. Price may trend directionally, but the distribution of volatility itself maintains structural balance.

Asymmetry emerges when downside volatility begins to dominate, cluster, or accelerate disproportionately. This signals regime stress—often before price structures visibly deteriorate. Asymmetric volatility increases execution risk at the microstructure level: fills degrade, slippage becomes unpredictable, and position stability erodes.

Systematic frameworks that ignore asymmetry often discover its presence only after risk controls have already been tested and breached.

Shock Persistence and Volatility Personality

The duration of elevated volatility after a disturbance matters more than the spike itself. Healthy regimes absorb shocks and normalize within predictable timeframes. Stressed regimes exhibit persistence: elevated volatility becomes self-reinforcing rather than mean-reverting.

Persistent volatility erodes the assumptions underlying execution quality, slippage models, and position-level stability. What appears as a temporary spike becomes a sustained shift in behavioral regime—one that static risk parameters were not designed to handle.

Recovery Elasticity Within Volatility Personality

Recovery elasticity measures how the system heals after volatility events. Does volatility compress smoothly back toward baseline? Does liquidity reappear proportionally? Do spreads re-tighten in an orderly manner?

Low elasticity environments often appear deceptively tradable while silently accumulating execution risk. The market may permit entry, but exit conditions have structurally deteriorated. By the time this becomes obvious, exposure has already been established under false assumptions.

The Volatility-Liquidity Coupling

Volatility personality does not act in isolation. Institutional market microstructure research consistently demonstrates that volatility behavior and liquidity response deteriorate together during stress conditions.

As volatility personality becomes asymmetric or persistent, observable changes occur across market structure:

- Depth thins at multiple levels

- Spreads widen non-linearly rather than proportionally

- Recovery becomes delayed, uneven, or incomplete

This coupling is documented in market microstructure analysis from the Bank for International Settlements (BIS), which shows that liquidity providers withdraw limit orders during periods of extreme volatility, spreads widen significantly, and trading volumes often decline precisely when execution quality matters most.

For behavior-first systems, volatility personality therefore acts as an early behavioral signal. Research demonstrates that a one standard deviation increase in volatility is associated with a 17% rise in liquidity costs, well before price patterns visibly reflect stress.

This coupling explains why volatility personality cannot be evaluated in isolation. Asymmetric volatility signals regime stress not only through price distribution, but through the simultaneous deterioration of liquidity response—depth, recovery speed, and spread behavior.

Why Static Risk Controls Fail Under Volatility Regime Shifts

Traditional risk management assumes volatility behavior remains stationary within defined bounds. Stops, position sizing rules, and drawdown limits are calibrated under that assumption.

When volatility personality shifts—when behavior changes rather than magnitude—static controls become structurally misaligned:

- Stops cluster and trigger simultaneously as volatility persistence invalidates spacing assumptions

- Position sizing becomes inappropriate as the relationship between size and execution risk changes non-linearly

- Loss distributions fatten unexpectedly as tail behavior deviates from calibration assumptions

Behavior-first trading avoids this failure mode by refusing to execute when volatility personality exits permissible bounds—before risk controls are tested. This represents a fundamental architectural difference: permission is withdrawn upstream of signal logic, not downstream through reactive controls.

This distinction separates infrastructure-grade frameworks from signal-centric approaches that rely on post-execution risk management.

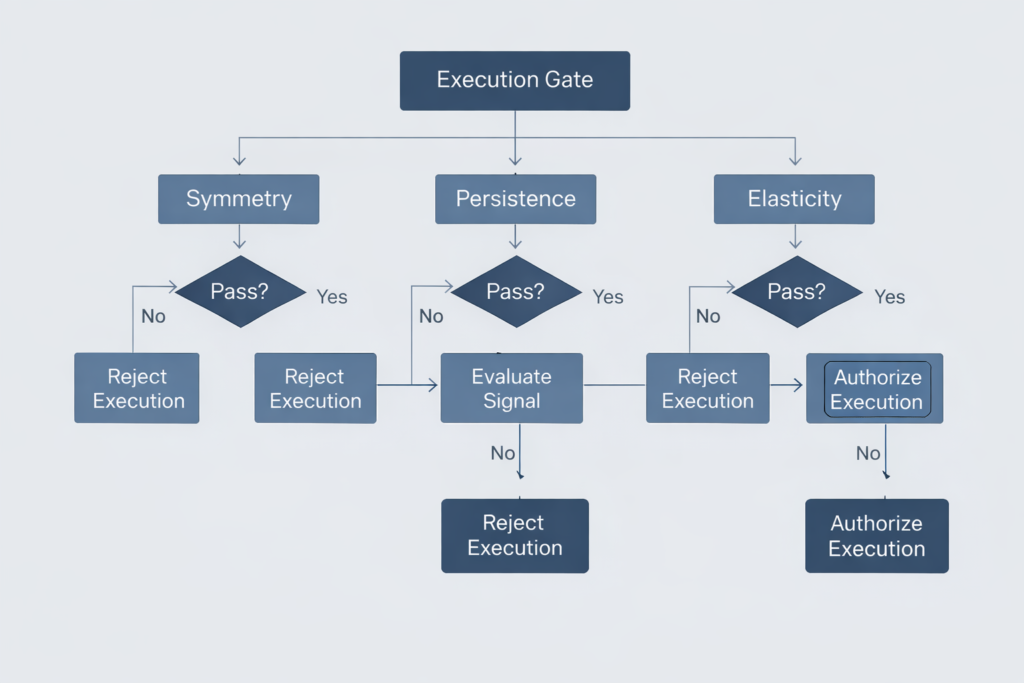

Volatility Personality as an Execution Gate

In systematic trading infrastructure, volatility personality functions as a permission gate rather than a forecasting input.

Execution logic activates only when volatility behavior demonstrates:

- Symmetric expansion within expected statistical ranges

- Bounded persistence with predictable decay characteristics

- Reliable recovery where volatility compresses smoothly and liquidity reappears proportionally

When these behavioral conditions fail, execution permission is withdrawn—regardless of whether signals remain statistically attractive, price trends continue, or opportunities appear present.

This approach prioritizes structural validity over opportunistic engagement. It recognizes that execution quality depends not on whether price might move favorably, but on whether the behavioral environment supports the assumptions embedded in execution logic.

Why Volatility Personality Explains Selective Inactivity

Selective inactivity often appears counterintuitive from a signal-centric perspective. Opportunities seem present. Price moves continue. Technical patterns fire.

But volatility personality may simultaneously indicate:

- Structural fragility beneath surface patterns

- Liquidity vulnerability that execution will reveal

- Elevated execution risk that position-level outcomes cannot overcome

In these conditions, inactivity is not risk avoidance or missed opportunity. It is system coherence—the preservation of behavioral alignment when market structure no longer cooperates with execution assumptions.

Behavior-first systems treat inactivity as a valid output, one that protects structural integrity rather than chasing statistical patterns divorced from execution reality.

Institutional Evaluation: Behavior Before Outcomes

Institutional evaluation frameworks do not begin with return metrics. They begin with behavioral questions:

- Did the system respect volatility regime boundaries?

- Did execution remain aligned with the behavioral assumptions underlying position management?

- Did exposure contract appropriately as volatility personality deteriorated?

- Were withdrawals of execution permission justified by subsequent regime behavior?

Performance fluctuates across environments. Behavior consistency must not.

This prioritization reflects how institutional capital protects long-duration compounding. Returns matter over multi-year horizons. But returns depend on behavioral discipline—on systems that recognize when their structural assumptions no longer hold and adjust exposure accordingly.

Volatility Personality Is Infrastructure, Not Insight

Volatility personality is not an indicator layered onto strategy logic. It is infrastructure classification—embedded upstream of signals, sizing rules, and execution decisions.

Without explicit volatility behavior classification, systems unknowingly assume stability. That assumption persists until it catastrophically fails—often during periods when execution conditions have already deteriorated but signal logic continues firing normally.

This is why behavior-first frameworks treat volatility personality as foundational input into environment classification and execution permission, not as a forecasting mechanism or alpha source.

The goal is not to predict where volatility is headed. The goal is to recognize whether current volatility behavior supports the structural assumptions that execution logic depends on.

The Relationship Between Volatility Personality and Market Structure

Volatility personality intersects directly with broader market microstructure dynamics. Research on market microstructure demonstrates strong empirical relationships between bid-ask spreads and volatility measures. A study published in Quantitative Finance examining order-driven markets found correlation coefficients (R²) exceeding 0.90 between spread and volatility per trade, suggesting that adverse selection is the main determinant of bid-ask spreads and that most volatility stems from trade impact.

Market structure analysis examines how order flow, depth, and spread behavior respond to volatility shifts. When volatility personality changes—becoming asymmetric or persistent—these microstructure elements deteriorate together. The depth thins. Spreads widen non-linearly. Recovery becomes delayed.

Additionally, research from the Bank for International Settlements on foreign exchange markets confirms positive correlation between bid-ask spreads and volatility, driven by inventory costs that widen when exchange rate volatility increases. This coupling explains why volatility personality cannot be evaluated in isolation from liquidity behavior.

Systematic frameworks that integrate volatility personality with market structure analysis gain clearer visibility into when execution conditions remain valid versus when they have silently degraded beneath acceptable thresholds.

Why Volatility Magnitude Alone Misleads

Two environments can exhibit identical volatility magnitude while differing completely in execution viability:

Environment A: High volatility, but symmetric, fast-decaying, with clean recovery. Execution remains structurally sound despite elevated magnitude.

Environment B: Moderate volatility, but asymmetric, persistent, with low recovery elasticity. Execution becomes unreliable despite lower magnitude.

Magnitude-based frameworks cannot distinguish these environments. They treat both as “high risk” or “medium risk” based purely on numerical thresholds.

Behavior-based frameworks recognize that Environment A may permit execution while Environment B does not—despite lower nominal volatility in the latter. This distinction becomes critical during regime transitions, where magnitude often lags behavioral deterioration.

Implementing Volatility Personality in Systematic Frameworks

Integrating volatility personality into systematic infrastructure requires upstream architectural decisions:

Classification Before Signal Evaluation

Volatility behavior must be classified before any signal logic executes. This prevents scenarios where signals fire normally while the behavioral environment has already exited permissible bounds.

The sequence becomes: (1) Classify volatility personality, (2) Evaluate execution permission, (3) If permission granted, proceed to signal evaluation. If permission denied, execution does not occur regardless of signal strength.

Dynamic Thresholds Rather Than Static Limits

Static volatility thresholds—”no execution above 20% annualized volatility”—ignore personality. A dynamic framework asks: Is expansion symmetric? Is persistence bounded? Is recovery elastic?

These questions cannot be answered with fixed numerical limits. They require behavioral classification that adapts to regime context.

Behavioral Consistency Over Opportunistic Engagement

The framework prioritizes behavioral consistency—maintaining structural alignment between execution logic and market behavior—over opportunistic engagement with statistically attractive patterns.

This requires accepting that periods will exist where signals fire but execution is denied. These periods are not system failures. They are the system functioning as designed: preserving behavioral integrity when market conditions no longer support execution assumptions.

The Link Between Volatility Personality and Risk Architecture

Risk architecture in systematic frameworks must account for volatility personality, not just magnitude. Traditional approaches size positions based on historical volatility or recent ranges. These methods assume behavioral stability.

When volatility personality shifts, position sizing rules calibrated under different behavioral assumptions become inappropriate. A position sized for symmetric, fast-decaying volatility becomes oversized when volatility turns asymmetric and persistent—even if magnitude remains similar.

Behavior-aware risk architecture adjusts exposure based on personality classification:

- Under symmetric, bounded behavior: Standard sizing applies

- Under emerging asymmetry: Sizing contracts preemptively

- Under persistent, low-elasticity behavior: Execution permission may be withdrawn entirely

This upstream adjustment prevents scenarios where risk controls are tested under conditions they were not designed to handle.

Volatility Personality Across Asset Classes

While the principles remain consistent, volatility personality manifests differently across asset classes:

Equity Indices: Asymmetry often emerges first. Downside volatility clusters before magnitude expands significantly. Persistence tends to be shorter-duration but more intense.

Fixed Income: Persistence matters more than asymmetry in stable regimes. Recovery elasticity deteriorates gradually during rate transition periods.

Currencies: Volatility personality often links to policy regime changes rather than market stress. Symmetry can break suddenly during intervention or major policy shifts.

Commodities: Shock persistence tends to be longer. Supply/demand imbalances create extended periods of elevated, persistent volatility with low recovery elasticity.

Understanding these asset-class differences allows systematic frameworks to calibrate personality classification appropriately while maintaining consistent behavioral principles.

Conclusion: Volatility Shapes Permission, Not Prediction

Volatility does not tell systems where price is moving. It tells systems whether they should be operating at all.

By shifting focus from volatility magnitude to volatility personality—from “how much” to “how it behaves”—systematic trading infrastructure ensures that execution decisions remain structurally aligned with real market behavior.

Strategies adapt. Signals change across environments. But volatility personality defines whether execution is structurally earned—whether the behavioral conditions exist that support the assumptions embedded in execution logic.

That is why volatility personality shapes every decision, long before the first trade exists. It is not an optimization layer. It is foundational infrastructure that determines when systematic frameworks engage and when they preserve integrity through disciplined inactivity.

Continue Learning About Behavioral Trading Infrastructure

Explore more research on behavior-first systematic frameworks and how market structure shapes execution decisions in institutional trading infrastructure.

About This Research

This article reflects ongoing research into systematic trading infrastructure and behavior-first frameworks. The principles outlined represent architectural approaches to execution permission and risk management, emphasizing structural alignment between market behavior and system assumptions. All content is educational and does not constitute investment advice or trading recommendations.