The Foundation of Environment-Based Trading

Environment-based trading reframes how systematic systems decide whether to operate before asking how to execute.

Most trading frameworks begin with a familiar question: where is price going next?

Environment-based trading begins somewhere else entirely. It asks whether the market environment itself is suitable for systematic execution—before any discussion of entries, targets, or signals.

This perspective aligns with how institutional trading infrastructure evaluates execution conditions: not through prediction accuracy, but through behavioural permission.

Why Environment-Based Trading Starts Before Opportunity

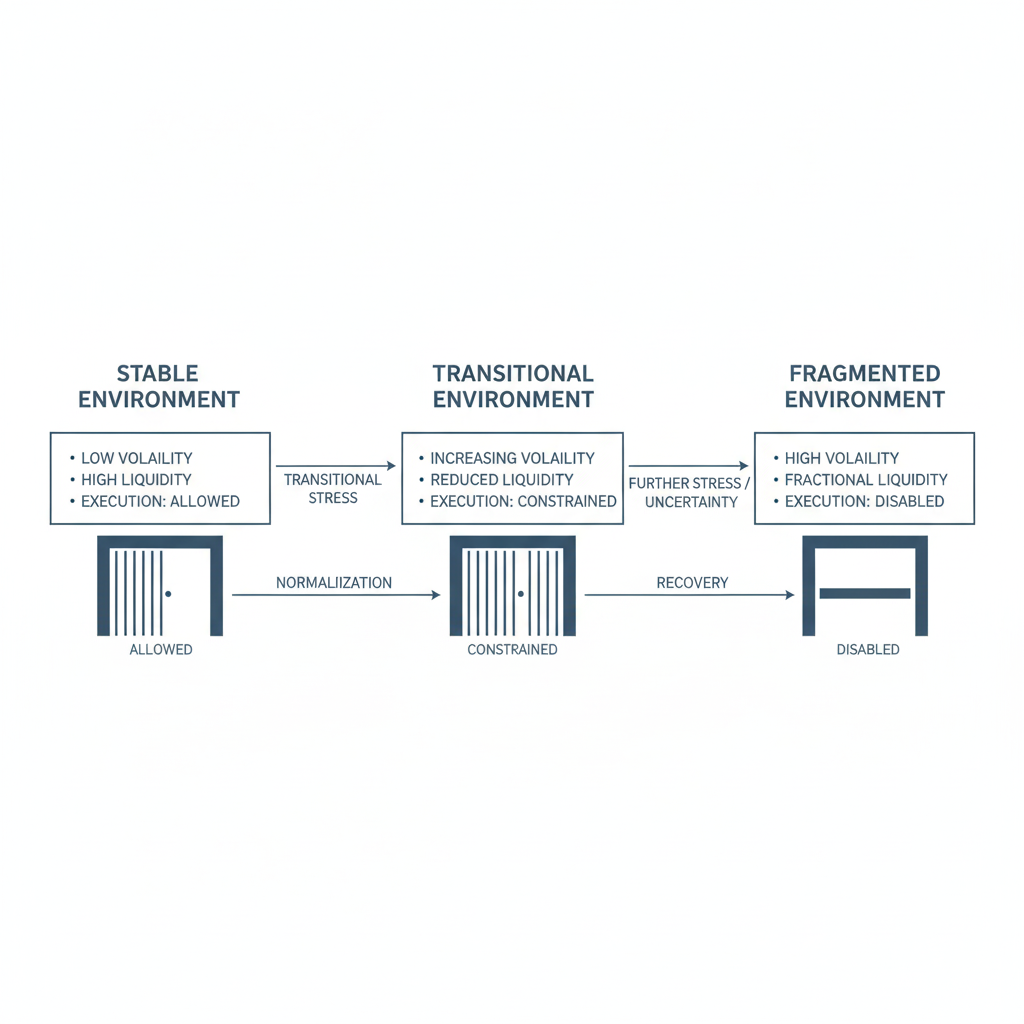

Markets do not behave uniformly. Volatility compresses and expands. Liquidity deepens and vanishes. Spreads tighten, then fracture. These shifts are not noise; they are signals about the state of the system itself.

Traditional retail frameworks tend to treat these conditions as background variables. The assumption is implicit:

If a pattern appears, execution is allowed.

Environment-based trading inverts that logic.

Execution is not assumed.

It is earned by the environment.

Only when volatility behaviour, liquidity response, and regime structure remain coherent does execution logic activate. When they deteriorate, the correct response is not adapting entries—it is inactivity.

This principle is consistent with the idea of behavioural coherence discussed in

System Integrity in Trading: Why It Matters More Than Performance

What Defines the Environment in Environment-Based Trading

In environment-based frameworks, an environment is not a vague macro label like “bull” or “bear.”

It is a measurable behavioural state composed of multiple interacting dimensions.

These dimensions collectively determine whether systematic execution is permitted.

Volatility behaviour → Liquidity response → Regime classification → Execution permission

1. Volatility Identity

Environment-based trading focuses not on volatility magnitude, but on volatility behaviour.

Systems examine whether upside and downside moves remain statistically symmetric, whether shocks decay or persist, and whether volatility normalises within expected bounds.

Persistent asymmetry or delayed normalisation signals regime instability—regardless of how attractive price action may appear.

2. Liquidity Behaviour

Liquidity is not static depth—it is response.

Healthy environments exhibit proportional spread expansion under pressure and rapid depth replenishment after impact. Deteriorating environments show vanishing depth, delayed recovery, or non-linear spread reactions that distort execution risk.

This behavioural view of liquidity aligns with institutional market structure analysis outlined in

Market Structure Analysis: Why Behavior Beats Prediction

3. Regime Coherence

Regimes are not predictions; they are classifications.

Environment-based trading evaluates whether current behaviour remains consistent with historically stable execution conditions. When coherence breaks, regime classification shifts—even if price trends appear intact.

These three dimensions form the environmental substrate upon which all execution logic depends.

Why Signal-First Logic Fails in Environment-Based Trading

Signal-first systems assume that price patterns are explanatory. Candles signal intention. Indicators forecast continuation or reversal. Risk controls are applied after execution, often statically.

The structural flaw is not that signals are “wrong.”

It is that they operate independently of environment validity.

During regime transitions—when volatility becomes asymmetric, liquidity fragments, or spreads widen disproportionately—signals may continue to appear statistically attractive. But the conditions under which those signals were historically valid no longer exist.

This phenomenon is well documented in market microstructure research from the

Bank for International Settlements (BIS), which shows that liquidity conditions and execution risk often deteriorate before price patterns visibly reflect stress, particularly during volatility regime transitions

(see BIS Quarterly Review on volatility behaviour and risk-taking dynamics):

Environment-Based Trading Is Not Risk Management

This distinction matters.

Risk management traditionally operates after execution decisions are made. Stops, sizing rules, and drawdown limits are applied assuming the trade itself was valid.

Environment-based trading operates before execution exists.

It does not attempt to manage risk within hostile environments.

It prevents execution into them.

Environment-Based Trading Prioritises Filtration Over Forecasting

One of the most counterintuitive principles in environment-based trading is that filtration creates more edge than forecasting.

Retail logic often equates opportunity frequency with edge. More trades mean more chances to win. Environment-based frameworks recognise the opposite: most long-term damage occurs during structurally invalid executions, not from normal variance.

By aggressively filtering environments—often rejecting the majority of apparent opportunities—systems preserve behavioural integrity across regimes.

Selective Inactivity as a System Output

In environment-based trading, inactivity is not a failure mode.

It is an explicit system output.

When volatility fragments, liquidity response deteriorates, or regime transitions accelerate, the correct action is often to do nothing. This is psychologically difficult for participants trained to equate activity with competence.

Systematic infrastructure cannot afford psychological bias.

It must respond only to environmental permission.

Why Environment-Based Trading Scales Institutionally

Institutional frameworks prioritise consistency over excitement. Capital longevity depends not on catching every move, but on avoiding catastrophic behavioural breakdowns.

Environment-based trading supports this priority because:

- Behaviour remains invariant even as performance fluctuates

- Execution rules remain stable across regimes

- Risk exposure contracts automatically during environmental stress

- Systems remain coherent when markets do not

This is why institutional evaluations typically examine behavioural profiles before performance summaries. Returns are outcomes; environments determine whether those outcomes were structurally earned.

Environment as Infrastructure, Not Insight

Environment-based trading is not a layer added to an existing strategy.

It is foundational infrastructure.

Signals, models, and execution logic operate within environments. Without an explicit environmental framework, systems implicitly assume stability—and that assumption eventually fails.

Dovest’s research direction reflects this understanding. The focus is not on improving prediction accuracy, but on formalising how environments are identified, classified, and enforced as execution constraints.

Conclusion: Markets Do Not Owe You Execution

Environment-based trading rests on a simple but demanding premise:

Markets do not owe participants execution opportunities.

Systems must earn permission through behavioural alignment.

By shifting focus from prediction to environment, from opportunity to permission, and from activity to integrity, environment-based trading establishes the foundation for systems that remain coherent across regimes.

Performance will fluctuate.

Environments will change.

Behavioural integrity must not.

That is the foundation upon which systematic infrastructure is built.