Market structure analysis is one of the most effective ways to understand how markets truly behave. Instead of focusing on forecasting price direction, market structure analysis examines the underlying environment — volatility patterns, liquidity dynamics, regime stability, and shock responses — to determine whether conditions support reliable, institutional-grade execution. This behaviour-first perspective forms the foundation of systematic trading integrity.

Across global markets, prices may appear random or unstable, but the environments behind them often follow consistent behavioural patterns. Structure, not prediction, explains these patterns. And understanding structure is essential for any system that aims to operate with discipline, transparency, and robustness.

1. Why Market Structure Analysis Matters

Prediction attempts to guess where price will go next.

Market structure analysis evaluates how the market behaves now.

For institutional systems, this shift is fundamental. Markets fail, systems break, and risk escalates not because predictions are wrong, but because the environment no longer supports the logic being used.

Market structure analysis provides clarity through:

- Behavioural classification

- Transparent decision-making

- Execution-aware context

- Stability vs instability detection

Prediction fluctuates.

Behaviour persists.

Structure reveals behaviour.

2. Core Components of Market Structure Analysis

To understand market structure, four behavioural domains must be observed together. Each component provides a different view of how markets form, absorb, and express information.

2.1 Volatility Identity

Volatility is not just magnitude — it is behaviour.

Volatility identity describes whether movement is:

- Stable or unstable

- Orderly or chaotic

- Compressing or expanding

- Noise-driven or structurally driven

These distinctions help determine when price behaviour aligns with systematic logic.

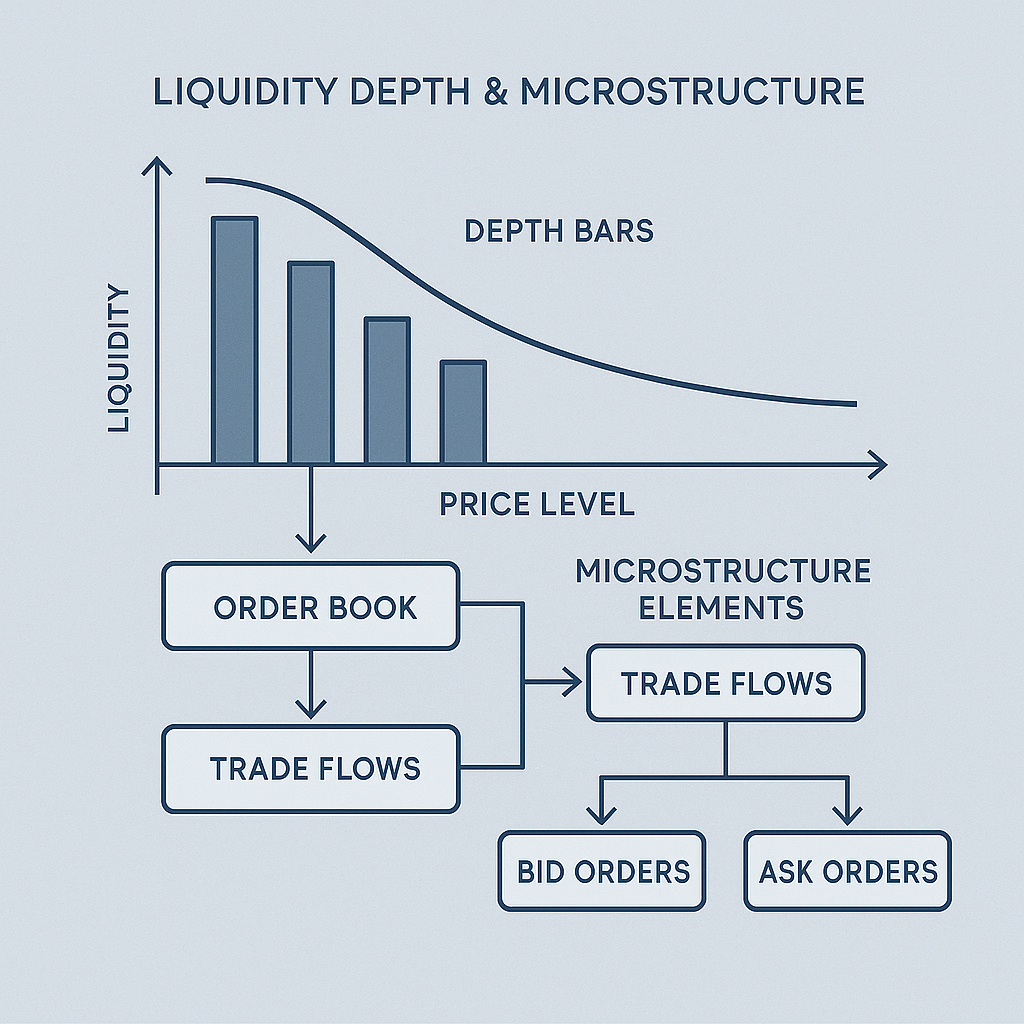

2.2 Liquidity Behaviour

Liquidity must be measured as a dynamic process, not a static number. Structural liquidity analysis observes:

- Spread stability under stress

- Depth replenishment behaviour

- Sensitivity to order flow

- Symmetry or fragmentation in participation

Two markets with identical spreads may behave completely differently during volatility. Structural analysis reveals this difference.

2.3 Regime Consistency

Markets rotate between behavioural regimes such as:

- Stable trend

- Controlled pullback

- Volatility expansion

- Fragmentation

- Shock-sensitive environments

Regime consistency determines whether current conditions support systematic logic. Systems fail not because models are flawed, but because they enter regimes their logic was never designed for.

2.4 Shock Absorption

How markets respond to stress is one of the strongest indicators of structural integrity. Key behaviours:

- Spread normalisation speed

- Depth rebuilding

- Volatility contraction patterns

- Persistence of micro-fractures

A market that absorbs shocks returns to equilibrium.

A fragile market amplifies them.

3. Why Market Structure Analysis Outperforms Prediction

Prediction is fragile to regime change.

Structure adapts to it.

3.1 Structure Is Explainable

Institutional systems must justify decisions.

Market structure analysis offers transparent logic:

- “Liquidity behaviour deteriorated.”

- “Volatility shifted to instability.”

- “Regime classification mismatched system design.”

Prediction cannot explain itself this clearly.

3.2 Structure Avoids Noise and Overfitting

Predictive models often fit historical price patterns that disappear under new conditions.

Structure-based frameworks avoid this because they rely on behaviour, not outcomes.

3.3 Structure Enables Consistent System Behaviour

Systems grounded in market structure analysis:

- Filter unsuitable environments

- Maintain rule integrity

- Avoid behavioural drift

- Adjust to regime conditions

- Remain stable across cycles

Consistency matters more than accuracy.

4. How Market Structure Analysis Supports System Integrity

System integrity is the measure of whether a system behaves as designed across environments.

4.1 Filtration Based on Structure

Filtering unsuitable conditions is a structural advantage, not a limitation.

When behaviour signals instability, systems step aside.

(A detailed framework on filtration logic will be introduced in a later article of this series.)

4.2 Behaviour-Based Risk Architecture

Risk is not just volatility — it is environment suitability.

Structural risk examines:

- Volatility identity

- Liquidity resilience

- Shock absorption

- Regime alignment

Risk becomes a behavioural truth, not an assumption.

4.3 Transparent Decision Logic

Institutions require explainable actions.

Structure provides decision paths grounded in observable facts.

4.4 Long-Term Robustness

By aligning operation with behavioural consistency rather than prediction, systems maintain robustness during:

- Volatility spikes

- Liquidity fragmentation

- Macro uncertainty

- Microstructure stress

Learn more about structural system integrity:

https://dovest.trade/blog/system-integrity-trading

5. Market Structure Analysis in Systematic Design

Market structure analysis informs:

- Environment taxonomy

- Filtration engines

- Execution-aware models

- Behaviour-first risk rules

- Regime transition detection

- Structural consistency checks

This framework supports systematic infrastructure that aligns with real market behaviour.

A full framework on behavioural environment classification will be introduced later in this series as Dovest expands its taxonomy of market states.

6. Common Misunderstandings About Market Structure Analysis

“Structure predicts direction.”

Structure identifies environment, not outcomes.

“It requires decades of performance data.”

Structural behaviour is visible independently of returns.

“Filtering means fewer opportunities.”

Filtering protects integrity.

“Liquidity equals spread width.”

Liquidity is behaviour, not appearance.

Conclusion

Market structure analysis reframes trading from predicting price movement to understanding market behaviour. It examines volatility identity, liquidity patterns, regime consistency, and shock response to classify environments with clarity and discipline.

Prediction is uncertain.

Structure is observable.

Prediction breaks under stress.

Structure explains why.

For institutions and systematic engineers seeking reliability, transparency, and behavioural integrity, market structure analysis is not optional — it is foundational.

Explore More Research on Behaviour-First Market Structure

A curated collection of research on structural environments, systematic design principles, and behaviour-first trading infrastructure.

About This Analysis

This article reflects Dovest’s institutional research perspective on market structure and systematic behaviour design.

Author: Dovest Research Team

Last Updated: Dec 2025

Disclaimer: Educational content only; not investment advice.

Outbound Research References

- Outbound Link 1 (BIS — Market Microstructure Research)

- 👉 https://www.bis.org/publ/qtrpdf/r_qt2409b.htm

- Outbound Link 2 (CFA Institute — Liquidity & Market Structure Studies)

- 👉 https://www.cfainstitute.org/research/macro/liquidity