Most trading advice is upside-shaped: find opportunity, refine entry, capture move. But scalable infrastructure begins with the opposite question: what is the downside the market can impose before any upside is even possible? That is the operational meaning of downside before upside—a market-structure rule that forces execution to be permitted by the environment, not justified by a pattern.

This article frames that rule through the market structure evaluation lens, with a sub-lens of environment permission: a disciplined way to decide when not to trade because the market’s mechanics are likely to penalize you—via slippage, adverse selection, or unstable liquidity—regardless of what price eventually does.

Market Structure Is the Hidden Constraint Behind Every Trade

Price Is Not the Execution Environment

Price is the headline. Execution is the reality. Market structure is the set of mechanisms that decides whether your intent can be expressed without being taxed into irrelevance: spreads, depth, fragmentation, queue priority, auction design, and how liquidity providers behave under stress.

The framework recognizes that execution quality depends on factors invisible to price charts. Bid-ask spreads widen unpredictably. Order book depth vanishes under pressure. Liquidity fragments across venues. These structural elements determine whether a theoretically sound idea can translate into a practically viable trade—a core principle explained in Behaviour-First Trading: Why Institutions Ignore Retail Logic

The Market’s Cost of Being Wrong Is Not Symmetric

Losses rarely come from being wrong in theory. They come from being wrong in the specific way the structure punishes: thin depth when you need liquidity, widening spreads when you need certainty, and one-way order flow when you need two-way markets.

Market microstructure research consistently demonstrates that execution costs spike during volatility precisely when trading opportunity appears most compelling. The structure imposes downside through mechanisms unrelated to directional accuracy: adverse selection against informed flow, inventory risk premiums from market makers, and impact costs that scale nonlinearly with urgency.

Why Scalable Systems Start With Constraints, Not Ideas

Retail logic scales ideas: “more setups,” “better entries.” Institutional logic scales constraints: “fewer valid environments,” “tighter permission gates.” The second approach is slower, less exciting—and far more survivable.

A behaviour-first framework does not optimize for finding more trades. It optimizes for maintaining operational integrity when the environment degrades. The system’s capacity to function under stress depends on recognizing when market structure no longer permits reliable execution—not on finding clever ways to trade anyway. This principle of System Integrity in Trading: Why It Matters More Than Performance defines how infrastructure scales responsibly.

Downside Before Upside: The Operational Rule

The Rule Stated Operationally

The rule is not philosophical. It is a sequencing requirement:

- Model the downside the structure can impose (even if direction is right)

- Require environment permission before checking opportunity logic

- Only then allow execution to occur

The purpose is to prevent the most common structural failure: trading in conditions where upside exists, but is not claimable at your execution quality.

This sequencing inverts conventional trading logic. Instead of asking “where is the opportunity?” and then managing risk, the framework asks “what structural damage can occur?” before considering whether opportunity is even relevant. Permission precedes evaluation.

What “Downside” Means in This Lens

In market structure, downside is not only price movement against you. It includes:

- Spread and re-quote risk (your edge converts to costs)

- Slippage and market impact (your size changes the outcome)

- Adverse selection (you trade when informed flow is dominating)

- Liquidity withdrawal (depth vanishes when volatility spikes)

- Microstructure noise (signals degrade because the tape changes character)

Each of these failure modes can render execution structurally invalid even when directional thesis proves correct. The market can move in your anticipated direction while simultaneously imposing costs that exceed any theoretical edge.

Upside Is Unreliable Without Downside Assessment First

Upside is easy to imagine because it’s visible on charts. But charts compress the real problem: how trades are filled. Market structure expands the real problem: why fills degrade—often exactly when “opportunity” looks most compelling.

Pattern recognition operates in price space. Execution operates in microstructure space. These spaces do not map linearly. A clean price pattern can coincide with fragile liquidity, one-way order flow, or spread instability—structural conditions that make the pattern untradeable regardless of its statistical properties.

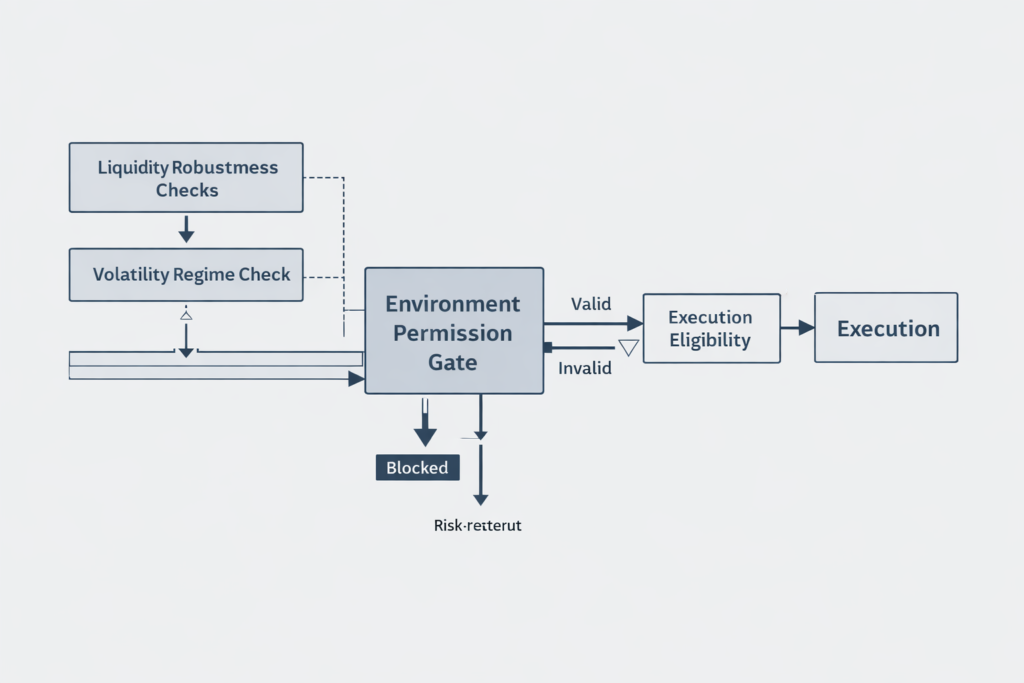

Environment Permission as the Gate Before Upside

Permission Is Not Prediction

Environment permission is not saying “the market will go up.” It is saying: “the structure is currently stable enough that execution is unlikely to be structurally invalid.”

This distinction separates forecasting from filtration. Forecasting attempts to predict future price. Filtration assesses whether current structure permits reliable execution. A system can have high conviction about direction while simultaneously lacking permission to act—because conviction addresses opportunity, not implementability.

Permission Is a Behaviour-First Concept

A behaviour-first system does not anchor on price narratives. It anchors on whether the environment supports consistent behaviour:

- Can orders be placed without chasing?

- Can stops be honoured without catastrophic gap risk?

- Can the expected friction stay within a known band?

If not, the correct action is structured inactivity.

The system’s behaviour must remain stable across varying market conditions. Permission logic ensures that the system only operates in environments where its designed behaviours can execute as intended. When the environment cannot support those behaviours, the system does not adapt—it stops.

Permission Is Earned, Not Assumed

A pattern can appear in any regime. Permission does not. Permission is conditional on the interaction between volatility and liquidity—how spreads react, how depth replenishes, how quickly the book reforms after prints.

Research from the Bank for International Settlements on market liquidity under stress emphasizes that liquidity is not a constant, especially during stress periods when market-making capacity can retract rapidly and transaction costs rise significantly. This conditional nature of liquidity means permission must be continuously re-evaluated rather than assumed from historical norms.

The Three Structural Failure Modes That Make “Good Ideas” Untradeable

Liquidity That Looks Present Until You Touch It

Displayed liquidity is not committed liquidity. In stressed conditions, quotes can be shallow, fleeting, or strategically placed. A system that scales must treat liquidity as a behaviour, not a number.

Order book depth represents posted intentions, not execution guarantees. Liquidity providers can cancel quotes faster than orders can be matched. Displayed size can be refreshed at different price levels rather than absorbed. What appears as consistent depth in market data feeds can evaporate the moment actual execution pressure arrives.

Volatility That Changes the Meaning of Every Signal

Volatility is not just “more movement.” It changes microstructure: spread dynamics, queue priority value, and the probability that your order becomes the market’s free option.

Higher volatility compresses the time value of limit order placement. It increases the adverse selection risk of passive orders. It changes the relative cost of market orders versus limit orders. The same technical pattern occurring in different volatility regimes represents fundamentally different execution environments, requiring different permission thresholds.

One-Way Order Flow That Turns You Into Inventory

When order flow becomes one-sided, the market forces someone to warehouse risk. If you are not explicitly designed to be that warehouse, you should not “help the market” by taking the wrong side at the wrong time.

Market makers expand spreads and reduce depth when order flow becomes directional. Taking the other side during these periods means accepting inventory risk without appropriate compensation. The structure effectively taxes liquidity provision through adverse selection—you systematically trade with better-informed counterparties.

The Downside-First Evaluation Stack Before Upside Assessment

Layer 1: Structural Friction Budget

Before signals, define what friction is acceptable:

- Max spread tolerance (relative, not absolute)

- Slippage band under normal conditions

- Impact sensitivity versus size

- Fill quality variance limits

If the structure cannot deliver fills within the friction budget, the trade is invalid even if direction later matches your thesis.

The friction budget establishes hard boundaries on acceptable execution degradation. These boundaries exist independently of opportunity assessment. A trade that violates friction tolerance fails structural validation regardless of its theoretical merit. This pre-commitment prevents the common failure mode of relaxing execution standards because “the opportunity is too good to miss.”

Layer 2: Liquidity Robustness Checks

Permission requires robustness, not just liquidity presence:

- Depth consistency (does it persist across prints?)

- Replenishment speed (does the book rebuild?)

- Spread stability (does it widen on small pressure?)

- Auction behaviour (open/close stability if relevant)

Static snapshots of order book depth provide incomplete information. Robustness assessment examines dynamic behaviour: how depth responds to executions, how quickly quotes replenish, whether spreads remain stable or deteriorate under normal trading pressure. Markets with fragile liquidity can appear deep in static measurement while exhibiting rapid degradation under stress.

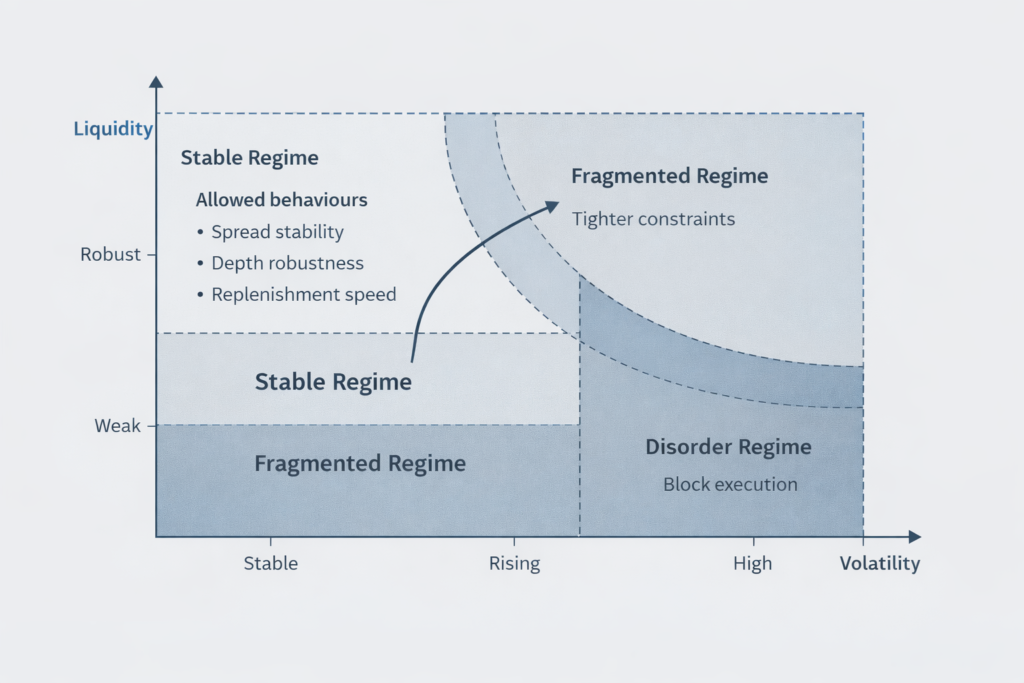

Layer 3: Volatility Regime Compatibility

Regimes are not for forecasting. They define allowed behaviours:

- In stable regimes, passive execution may be viable

- In fragmented regimes, only strict filters and smaller size may be permissible

- In disorder regimes, execution might be blocked entirely

Volatility regime classification determines which execution behaviours remain structurally valid. This is not risk sizing based on volatility forecasts. It is behaviour gating based on observed volatility characteristics. Different regimes permit different actions—not because risk preferences change, but because the environment’s capacity to support execution changes.

Layer 4: Only Then—Opportunity Evaluation

Opportunity is last because it is the least reliable part of the chain. It is cheap to generate, expensive to execute.

Signal generation operates at low marginal cost. Ideas are abundant. Execution operates at structural cost determined by market mechanics. The downside-first stack reflects this asymmetry: eliminate structurally invalid conditions before investing effort in opportunity assessment. Most potential trades fail structural validation, making opportunity evaluation unnecessary.

What Market Microstructure Teaches About Downside Before Upside

Liquidity Is Conditional, and It Can Disappear Quickly

Institutional research repeatedly emphasizes that liquidity is not a constant—especially during stress. When volatility rises or balance sheet constraints bite, market-making capacity can retract and costs rise.

The CFA Institute research on liquidity in equity markets documents how market quality can degrade through multiple channels: wider spreads, reduced depth, increased price impact, and higher volatility. These degradations are not uniform—they concentrate in specific instruments and time periods, creating execution environments fundamentally different from normal conditions.

Liquidity provision depends on market makers’ capacity and willingness to hold inventory. Both factors compress during stress. Regulatory capital requirements, risk limits, and funding costs all constrain market-making capacity precisely when demand for liquidity increases. During severe stress, counterparty risks and liquidity constraints become of first-order importance, creating conditions where liquidity can disappear exactly when execution need is highest.

Structural Risk Is Often Invisible in Calm Backtests

Backtests often assume fill simplicity. Market structure reminds us that the worst outcomes arrive when the distribution of execution quality changes—wider spreads, thinner depth, delayed fills. That is precisely when downside expands before upside can be realized.

Historical simulation typically uses midpoint pricing or simple spread assumptions. Real execution faces dynamic costs: spread width varies with volatility, market impact scales with urgency, and fill probability depends on order flow toxicity. These factors remain stable during calm periods but deteriorate rapidly during stress—creating a gap between backtested performance and live execution exactly when it matters most.

The Practical Implication of Downside-First Logic

A downside-first rule is not pessimism. It is acknowledging that the market’s mechanics can turn a theoretically “right” trade into a systematically losing behaviour.

Correctness in market structure terms means maintaining execution integrity, not predicting direction accurately. A system can be directionally correct while structurally wrong—taking profitable price moves while experiencing negative implementation shortfall due to execution costs. The downside-first framework prioritizes structural correctness because it determines long-term viability independent of directional skill.

Implementation Principles for Downside Before Upside

Define “Invalid Execution” Explicitly

Scalable infrastructure must formalize what invalid looks like:

- Excessive spread widening relative to normal

- Depth instability (quotes vanish on small pressure)

- Slippage beyond tolerance bands

- Increased gap probability around structural events (auctions, news windows, rebalances)

An invalid execution is not a “bad trade.” It is a trade that should not exist in the system.

Invalidity criteria must be specified in advance and enforced mechanically. Subjective assessment of “acceptable” execution quality leads to criterion drift under pressure—standards relax when opportunity appears compelling. Pre-committed invalidity thresholds prevent this drift by treating structural violation as a hard constraint rather than a discretionary judgment.

Separate Research Thresholds From Live Thresholds

A research-grade framework can explore a wider range of environments. A deployment-grade framework typically needs tighter gates. The key is transparency: thresholds exist to protect behaviour, not to optimize excitement.

Research operates in exploratory mode, testing boundary conditions and edge cases. Live operation requires conservative thresholds that preserve system integrity under unexpected conditions. This separation prevents research curiosity from contaminating operational discipline. The system in production runs only within well-characterized structural environments, even if research investigates broader possibility space.

Design for “No-Trade” as a First-Class Output

No-trade is not a failure state. It is an engineered output:

- If permission is missing, the system does not negotiate

- If permission is borderline, the system tightens behaviour rather than “hoping”

- If permission returns, the system re-enables execution without emotional residue

This is where downside before upside becomes practical: downside defines the boundary; upside is optional.

A well-designed systematic framework spends most of its time inactive. Activity occurs only when structural conditions satisfy permission requirements—a minority of total time. The system treats inactivity as success in maintaining behavioural standards rather than failure to find opportunity. This reframing is essential for operational stability.

Common Misunderstandings About Downside Before Upside Logic

“But the Move Happened—So the Filter Was Wrong”

A filter is not a predictor. Missing a move can be correct if the environment made execution structurally unreliable. Systems that chase “being right” often become structurally fragile.

Opportunity cost is not the same as structural cost. Missing upside that could not have been reliably captured is not an error—it is the filter functioning as designed. The system optimizes for long-term behavioural integrity, not short-term opportunity capture. This requires accepting that many profitable price moves will occur outside permissible structural conditions.

“I Can Just Reduce Size in Bad Conditions”

Sometimes. But size reduction is not a universal fix. Some regimes punish even small orders via spread spikes, gaps, or adverse selection. Permission is about quality of the environment, not only quantity of risk.

Structural invalidity affects execution quality per unit of size, not just aggregate exposure. A small order in a structurally invalid environment still faces disproportionate costs: adverse selection, spread crossing at unfavorable levels, impact that moves the market despite modest size. Position sizing addresses exposure management. Permission gating addresses structural viability.

“This Sounds Like Over-Filtering”

Over-filtering is a retail fear. Institutional risk architecture is comfortable with scarcity—because it understands that most long-term damage comes from a small number of structurally invalid periods.

Frequency is not the objective. Consistency is. A system that trades rarely but maintains structural discipline will outperform a system that trades frequently with occasional structural violations. The mathematics of compounding favours avoiding catastrophic periods over maximizing activity. Downside-first logic accepts lower frequency as the cost of structural reliability.

Why Downside Before Upside Scales Across Assets and Timeframes

Market Structure Generalizes Better Than Patterns

Patterns change. Market structure persists as a set of constraints: transaction costs, depth behaviour, participant incentives. Even as venues evolve, the principle remains: execution quality is conditional.

Technical patterns exhibit regime dependence and degradation over time as they become known and exploited. Market structure constraints remain relatively stable because they derive from fundamental limitations: information asymmetry, inventory risk, search costs, and coordination problems. These constraints transcend specific market regimes or asset classes.

A Scalable System Is One That Degrades Gracefully

When conditions worsen, a scalable system should:

- Reduce behavioural complexity

- Tighten permission gates

- Preserve capital and behavioural consistency

It should not “try harder.”

Graceful degradation means the system’s response to worsening conditions is predetermined and mechanical. As structural quality declines, permitted behaviours narrow progressively until reaching full inactivity if necessary. The system does not attempt to compensate for poor conditions through increased activity, tighter stops, or relaxed filters—responses that typically accelerate degradation.

Behaviour-First Scaling Is Not Volume-First Scaling

Scaling is not increasing trades. Scaling is maintaining integrity as constraints tighten. That is why downside-first logic is foundational: it protects the system when the environment becomes hostile.

True scaling means the system’s core behaviours remain unchanged as capital increases, time horizon extends, or market conditions vary. Volume increase is a byproduct of finding additional structurally valid environments, not an objective achieved by loosening standards. The downside-first framework scales because structural validation criteria remain constant regardless of opportunity pressure.

A Practical Checklist for Market-Structure Permission

Permission Questions to Ask Before Opportunity

Use these as research prompts—not retail “signals”:

- Are spreads stable relative to recent norms?

- Is displayed depth persistent or fleeting?

- Does liquidity replenish after prints?

- Is order flow two-way or one-sided?

- Is volatility regime compatible with the system’s allowed behaviours?

These questions assess structural quality, not directional opportunity. They examine the market’s capacity to support execution, not its likely direction. Each question addresses a specific failure mode: spread stability prevents cost explosion, depth persistence prevents liquidity mirages, replenishment speed indicates genuine market-making commitment, order flow balance prevents adverse selection, regime compatibility ensures behavioural validity.

If You Cannot Answer, You Cannot Justify Execution

Uncertainty is not an invitation to act. In infrastructure, uncertainty is a reason to tighten constraints until the system’s behaviour remains defensible.

Missing data or ambiguous structural signals constitute negative permission—absence of confirmation rather than neutral information. The system requires positive permission: clear evidence that structural conditions satisfy requirements. Ambiguity defaults to inactivity because the cost of trading in uncharacterized conditions exceeds the opportunity cost of waiting for clarity.

Where CFA-Style Market Quality Thinking Fits

Market Quality Is a Structural Concept

Market quality is not a feeling. It is observed through costs, transparency, fragmentation effects, and liquidity characteristics—especially during stress and complexity.

The CFA Institute framework for market quality assessment provides systematic methodology for evaluating execution environments. It emphasizes measurable indicators: effective spreads, price impact, depth resilience, and volatility during stress. These metrics quantify the structural characteristics that determine whether a market can support reliable execution.

The Infrastructure Takeaway

When market quality degrades, strategies do not simply “perform worse.” They can become structurally invalid if execution assumptions break. A downside-first rule treats that invalidity as a hard stop, not a drawdown you “fight through.”

Performance degradation differs fundamentally from structural invalidity. Performance degradation implies the system continues functioning with reduced returns. Structural invalidity means the system’s execution mechanism has broken—fills occur at prices that invalidate the original logic, or execution uncertainty becomes large relative to expected edge. The downside-first framework distinguishes these cases and responds appropriately: accept performance variation, but cease operation during structural breakdown.

Conclusion: The Discipline Is in the Order of Operations

The most scalable trading rule is not “find better upside.” It is define and contain downside before evaluating upside—because market structure decides what you can actually capture, and environment permission decides whether you should attempt capture at all.

In a behaviour-first framework, this sequencing is non-negotiable:

- Behaviour > Price

- Structure > Prediction

- Integrity > Excitement

- Engineering > Signals

- Risk > Returns

When systems respect that order, they become less reactive, less fragile, and more consistent in the only way that matters: they behave the same way when the market stops cooperating.

The downside before upside principle is not a risk management overlay applied after strategy design. It is the foundational logic that determines what strategies can exist within the system. By inverting conventional sequencing—assessing structural constraints before evaluating opportunity—the framework builds reliability into system architecture rather than depending on discretionary discipline during operation.

This approach sacrifices frequency and excitement. It gains something more valuable: the capacity to maintain operational integrity when market structure degrades. That capacity distinguishes systems that survive extended deployment from those that work only in benign conditions.

Follow the Upcoming Series on Structure-First System Design

Dovest publishes research on systematic trading infrastructure with a behaviour-first approach—focused on market structure, filtration, and risk architecture. Our goal is to clarify how execution constraints and environmental conditions shape what a system can responsibly do, and just as importantly, when it should do nothing.

Author: Dovest Research Team

Dovest publishes research on systematic trading infrastructure with a behaviour-first approach—focused on market structure, filtration, and risk architecture. Our goal is to clarify how execution constraints and environmental conditions shape what a system can responsibly do, and just as importantly, when it should do nothing.