Why Dovest Rejects Retail Logic: Behaviour Over Charts

Most retail trading begins with the same foundational assumption: price patterns contain predictive information. Charts display setups. Indicators signal entries. Patterns suggest continuation or reversal. Behaviour-first trading rejects this entirely. Instead of asking where price might move, behaviour-first trading systems examine how markets function under varying conditions. This distinction is not stylistic—it fundamentally redefines strategy architecture, risk management, and execution logic. Retail systems optimize for prediction. Institutional frameworks optimize for structural integrity.

Understanding why institutions prioritize behaviour over charts requires examining what markets actually reveal through price action, how behaviour-first trading systems process information differently, and why this approach aligns with systematic trading infrastructure rather than discretionary retail logic.

Why Price Patterns Fail in Behaviour-First Trading

Retail trading logic treats charts as explanatory mechanisms. Candlestick formations signal trader intention. Support and resistance levels indicate boundaries. Breakouts imply momentum continuation. Mean reversion strategies assume prices return to equilibrium.

These interpretations share a critical flaw: they treat price as an output rather than an input.

Price aggregates thousands of decisions across diverse participants operating under different information sets, time horizons, and risk constraints. A candlestick pattern does not explain why liquidity dried up at a specific level. A breakout does not reveal whether the move occurred in a stable regime or during a structural shift. Charts compress complex system behaviour into simplified visual representations.This limitation becomes critical during regime transitions. Research from the Bank for International Settlements demonstrates that market behaviour patterns change dramatically when liquidity conditions shift, with participant exits potentially cascading into market halts, yet retail chart patterns cannot distinguish between stable and unstable regimes. A bullish engulfing candle appears identical whether formed during normal liquidity or during a structural breakdown.

Behaviour-first trading addresses this directly by treating price as secondary information—an output generated by underlying system dynamics rather than a causal factor itself.

What Behaviour-First Trading Systems Actually Measure

Rather than interpreting price patterns, behaviour-first trading quantifies observable market characteristics that indicate system health. These measurements fall into distinct categories that institutional frameworks monitor continuously.

Volatility Behaviour in Systematic Trading Analysis

Volatility behaviour examines not just magnitude but symmetry, persistence, and response patterns. A volatility spike during normal trading hours with rapid mean reversion indicates different system conditions than sustained elevated volatility with asymmetric distribution. The latter suggests structural stress regardless of what chart patterns appear.

Behaviour-first systems measure:

- Volatility symmetry: Whether upside and downside moves exhibit similar statistical properties

- Shock persistence: How long abnormal volatility persists after events

- Recovery elasticity: The speed and character of volatility normalization

These measurements quantify regime stability. Charts cannot.

Liquidity Depth Assessment in Behaviour-First Trading

Liquidity behaviour reveals how markets absorb order flow under varying conditions. Microstructure research demonstrates that transaction activity patterns in markets link directly to implicit spread behaviour and depth characteristics, creating environments where seemingly attractive chart setups become structurally dangerous.

Behaviour-first trading monitors bid-ask spread dynamics, order book depth at multiple price levels, and how these metrics respond to order flow pressure. A market exhibiting healthy liquidity shows spreads that compress during normal trading and widen proportionally during stress. When spreads explode disproportionately or depth vanishes at critical levels, the system flags a regime change—before chart patterns have time to form recognizable signals.

Spread Expansion Versus Compression

The relationship between spread behaviour and transaction volume provides critical information about market capacity. During stable regimes, increased volume corresponds with spread compression as liquidity providers compete for flow. During stressed regimes, volume increases coincide with spread expansion as providers withdraw capital.

This dynamic cannot be assessed through price charts alone. Two identical candlestick patterns can form under completely opposite liquidity conditions, yet only one represents executable opportunity within institutional risk parameters.

Why Retail Signals Break During Regime Shifts

Retail trading signals optimize for pattern recognition within assumed stable conditions. Moving average crossovers, RSI divergences, and Fibonacci retracements all depend on implicit assumptions about market behaviour remaining consistent.

When regime shifts occur—volatility fragments, liquidity fractures, or correlation structures break—these assumptions become invalid. The signals continue generating entries, but the underlying conditions have fundamentally changed.

The Assumption Drift Problem in Retail Trading

Retail systems suffer from what can be termed assumption drift: the gradual or sudden invalidation of assumptions upon which signals were optimized. A mean reversion strategy assumes price will return to a statistical mean. This assumption holds during range-bound regimes but fails catastrophically when trends establish or volatility regimes shift.

Behaviour-first trading eliminates assumption drift by measuring the validity of assumptions continuously. Rather than assuming mean reversion works, the system verifies whether current behaviour exhibits mean-reverting characteristics. When behaviour shifts, filtration layers halt execution regardless of what signals indicate.

Signal Stacking Without Behavioural Context

Many retail approaches stack multiple indicators to increase confidence. A trade receiving confirmation from RSI, MACD, and volume indicators appears robust. Yet if all indicators derive from the same price data without behavioural context, they provide redundant rather than independent confirmation.

During regime transitions, correlated indicators fail simultaneously because they all miss the underlying shift in market structure. Behaviour-first frameworks avoid this by measuring independent dimensions: volatility symmetry, liquidity depth, and stress response are structurally different measurements that cannot simultaneously fail from the same cause.

Institutional Risk Architecture in Behaviour-First Trading

The distinction between behaviour-first trading and retail logic becomes most apparent in risk architecture. Retail systems typically employ static stop losses, fixed position sizing, and predetermined risk-reward ratios. These tools assume markets behave within known boundaries.Institutional frameworks recognize that systemic risk refers to cascading failures within interconnected financial systems, requiring dynamic rather than static risk controls. Behaviour-first trading implements this understanding through regime-aware risk architecture.

Dynamic Position Sizing Based on Market Behaviour

Rather than applying fixed position sizes across all market conditions, behaviour-first systems adjust sizing based on observed regime characteristics. During stable regimes with symmetric volatility and healthy liquidity, position sizes operate at normal parameters. When behaviour indicators flag regime stress, sizing reduces automatically—potentially to zero.

This creates a fundamental difference from retail logic. Retail traders typically maintain consistent position sizes until stopped out. Institutional systems reduce exposure preemptively when behaviour deteriorates, even before losses occur.

Invariant Risk Parameters

The term “invariant” in institutional risk management means risk controls that do not change based on performance. A retail trader experiencing a winning streak might increase position sizes, believing they have identified an edge. During losing periods, they might reduce sizes or stop trading entirely.

Both responses introduce behavioural inconsistency. Behaviour-first systems maintain invariant risk parameters: position sizing logic remains constant across winning and losing periods. What does change is the system’s willingness to execute based on environmental behaviour rather than recent results.

Structure Over Prediction: Core Philosophy of Behaviour-First Trading

The fundamental distinction between behaviour-first trading and retail logic extends beyond methodology into philosophy. Retail approaches optimize for prediction accuracy. Institutional frameworks optimize for structural soundness.

Prediction Requires Forecasting Price Direction

Retail systems inherently assume that predicting price movement is possible and profitable. Technical analysis attempts to forecast direction through pattern recognition. This assumption places the entire framework on unstable ground—not because forecasting is impossible, but because forecasting accuracy varies by regime.

During trending regimes, momentum indicators predict continuation with reasonable accuracy. During range-bound regimes, mean reversion strategies forecast reversals effectively. The critical flaw: retail systems cannot reliably identify when regime conditions have shifted, making their predictions valid one moment and invalid the next.

Structure Measures System Integrity in Behaviour-First Trading

Behaviour-first trading rejects the prediction requirement entirely. Instead of forecasting price movement, these systems measure whether market structure remains within acceptable bounds for execution. The question is not “where will price go?” but rather “is the market behaving in a way that permits systematic execution?”

This distinction eliminates regime-dependent assumptions. Structural measurements—volatility symmetry, liquidity depth, spread behaviour—remain valid across different market conditions. When structure deteriorates, the system halts regardless of what directional forecasts might suggest.

Why Institutions Evaluate Behaviour Before Performance

In many institutional evaluations, the primary focus is not on headline outcomes but on how a system behaves across different market environments. This emphasis reflects a structural reality: outcomes fluctuate, while behavioural consistency determines whether a framework can remain viable over time.

Performance varies naturally as market conditions change. What matters more is whether volatility behaviour, drawdown structure, and risk controls remain coherent when conditions shift. Systems that preserve these characteristics demonstrate discipline at the architectural level, independent of short-term outcome variability.

By contrast, frameworks that appear attractive based on results alone can mask deeper weaknesses. Inconsistent drawdown structures, regime-dependent volatility responses, or position sizing that adapts to recent outcomes rather than observed conditions raise concerns in institutional contexts. These patterns suggest that the system’s behaviour is unstable, even if recent outcomes appear favourable.

Behavioural Integrity Under Stress

Market stress is where structural assumptions are most clearly tested. Behaviour-first frameworks are designed to remain coherent under stress by prioritising regime awareness, liquidity sensitivity, and risk gating principles over reactive decision-making.

Rather than relying on static rules or discretionary adjustments, behaviour-first approaches emphasise predefined responses to changes in market behaviour. When volatility fragments, liquidity deteriorates, or stress responses become asymmetric, execution eligibility tightens automatically. This does not imply immunity to adverse conditions; it reflects an architectural intent to prevent behaviour from drifting when environments become unstable.

From an institutional perspective, this distinction is critical. Systems are not evaluated on their ability to perform well only when conditions are favourable, but on their capacity to maintain behavioural integrity when conditions deteriorate. A framework that preserves discipline during stress is structurally different from one that depends on market cooperation to function as intended.

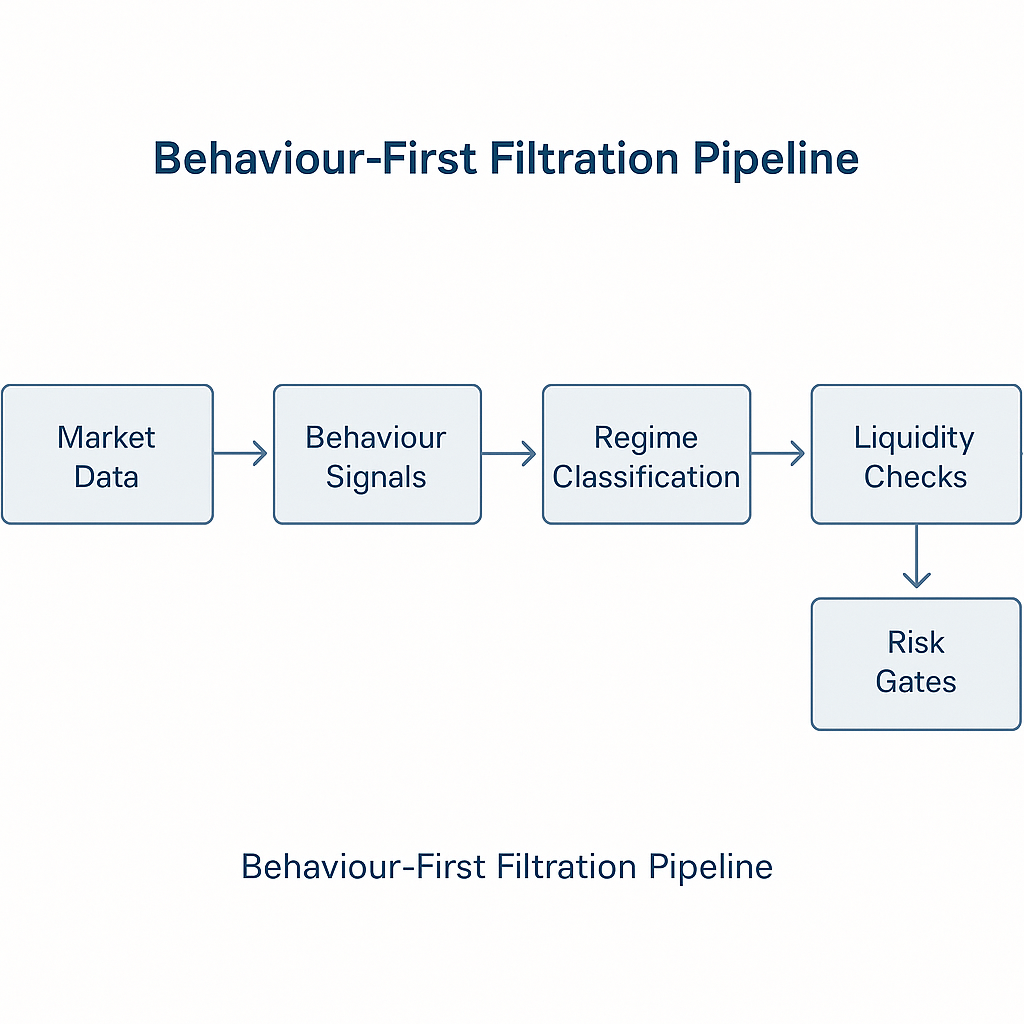

Implementing Behaviour-First Trading: Practical Framework Components

Transitioning from retail to behaviour-first trading requires rebuilding strategy architecture from the foundation. This process involves several distinct components that work in coordination.

Regime Classification Layer

The first component assesses current market regime characteristics. This layer does not predict which regime will occur next but identifies which regime currently exists. Classification criteria include volatility symmetry, trend coherence, and correlation stability.

During stable regimes, these metrics exhibit consistent patterns. Volatility remains symmetric across upside and downside moves. Correlations between related instruments maintain stability. Trends show coherent directional movement without erratic reversals.

When any classification metric deteriorates beyond acceptable thresholds, the system flags a regime transition. This flag does not prevent trading but triggers heightened scrutiny in subsequent filtration layers.

Liquidity Assessment Layer in Behaviour-First Systems

After regime classification, the system evaluates whether current liquidity conditions permit systematic execution. This assessment examines spread behaviour, order book depth, and volume profiles.

Healthy liquidity exhibits specific characteristics: spreads compress during normal flow, depth replenishes quickly after fills, and volume patterns remain consistent with historical norms. When these characteristics deteriorate—spreads widen disproportionately, depth vanishes at key levels, or volume becomes erratic—the system reduces exposure or halts execution.

This layer prevents the common retail mistake of executing into illiquid markets because a chart pattern looks attractive. Price patterns cannot reveal liquidity conditions, but behaviour measurement can.

Stress Response Validation

Even when regime classification and liquidity assessment pass initial checks, the system must verify how markets respond to stress. This validation examines shock absorption capacity and recovery patterns.

Markets exhibiting healthy stress response absorb volatility spikes without cascading effects. Price impact from large orders remains proportional. Recovery from shocks occurs smoothly rather than through further fragmentation.

When stress response deteriorates, the system recognizes that normal risk parameters no longer apply. Execution logic may remain theoretically sound, but implementation becomes structurally hazardous.

The Performance Paradox in Behaviour-First Trading

One of the most counterintuitive aspects of behaviour-first trading involves rejecting profitable opportunities that violate behavioural criteria. A retail trader executing a setup that generates profit has achieved their primary objective. An institutional framework evaluating the same scenario might classify the trade as a failure despite positive returns.

Structural Violations Versus Profitable Outcomes

Consider a scenario where regime classification indicates elevated stress, liquidity assessment shows deteriorating depth, yet a chart pattern suggests strong directional opportunity. A retail system executes because the setup meets signal criteria. The trade generates profit.

From a behaviour-first perspective, this represents a structural violation. The system executed outside acceptable behavioural bounds. That the trade happened to be profitable is incidental—the next similar execution under equivalent conditions might result in catastrophic loss because the behavioural foundation was unsound.

Institutional frameworks prioritize process integrity over outcome optimization. A losing trade that maintained behavioural discipline is acceptable. A winning trade that violated structural criteria represents system failure requiring correction.

Why Retail Logic Cannot Scale Institutionally

This philosophical divide explains why retail trading approaches rarely scale to institutional size. Retail logic optimizes for individual trade outcomes. As capital grows, this optimization becomes increasingly fragile.

Institutional frameworks recognize that edge exists not in predicting individual trade outcomes but in maintaining consistent process across thousands of iterations. Behaviour-first architecture ensures that every execution meets structural criteria, creating reliable long-term characteristics even when short-term results vary.

Market Structure Analysis in Behaviour-First Trading Frameworks

Understanding the distinction between behaviour-first trading and retail logic requires examining what each approach actually analyzes. Retail traders analyze charts—visual representations of price history. Institutional frameworks analyze market structure—the underlying mechanics that produce price movements.

What Charts Cannot Reveal

Charts display price, volume, and time relationships. They cannot show:

- Liquidity distribution across price levels

- Order flow dynamics creating price movements

- Participant composition driving volume patterns

- Structural fragility preceding breakdowns

- Regime transitions before they fully manifest

These hidden dimensions determine whether apparent opportunities represent genuine edge or structural traps. Behaviour-first systems measure these dimensions directly rather than inferring them from price patterns.

What Market Structure Reveals

Market structure analysis examines the mechanics underlying price formation. This includes spread dynamics, depth profiles, transaction cost evolution, and how these elements respond to varying conditions.

When market structure remains healthy, systematic execution can proceed with known risk parameters. When structure deteriorates—spreads become unstable, depth concentrations shift, transaction costs spike unpredictably—the system recognizes that execution risk has fundamentally changed regardless of what chart patterns suggest.

This structural awareness provides the foundation for institutional risk management. Rather than reacting to losses after they occur, behaviour-first systems prevent execution when structural conditions indicate elevated danger.

Why Dovest Prioritizes Behaviour-First Trading Principles

The Dovest framework exemplifies behaviour-first trading principles applied to systematic infrastructure. Rather than building around signal generation or pattern recognition, the architecture prioritizes behavioural measurement, structural filtration, and regime-aware execution.

This design reflects understanding that sustainable systematic trading requires:

Environmental Assessment Before Opportunity Evaluation: Markets must first be deemed suitable for execution before any trade consideration occurs. This inverts retail logic, which evaluates opportunities first and considers environment secondarily.

Structural Integrity Over Performance Optimization: System design emphasizes maintaining consistent behavioural characteristics rather than maximizing returns. This ensures long-term reliability even when short-term results vary.

Dynamic Risk Architecture Over Static Controls: Risk parameters adjust based on observed behaviour rather than remaining fixed. This adaptation prevents the common failure mode where static controls prove inadequate during regime transitions.

Process Discipline Over Outcome Fixation: Success is measured by adherence to behavioural criteria rather than individual trade outcomes. This creates systematic consistency rather than outcome-dependent decision-making.

These principles distinguish institutional frameworks from retail approaches. Retail logic asks what price will do. Behaviour-first trading asks whether current conditions permit systematic execution with acceptable structural risk.

Read more about this in our article on system integrity in trading, which explores how structural discipline supersedes performance metrics.

The Systematic Edge: Consistency Through Behaviour-First Trading

The ultimate advantage of behaviour-first trading emerges not from superior prediction but from systematic consistency. Retail traders experience performance volatility because their edge depends on pattern recognition accuracy, which varies by regime. Institutional frameworks generate consistency because their edge derives from behavioural discipline, which remains valid across regimes.

Edge Through Filtration, Not Prediction

Retail systems build edge through identifying setups with positive expectancy. This requires accurately predicting which patterns will resolve favorably more often than they fail. When regime conditions shift, historical pattern reliability degrades, eliminating edge.

Behaviour-first systems build edge through rigorous filtration. By refusing execution when behavioural criteria are not met, these frameworks avoid the catastrophic trades that destroy retail accounts. Edge comes not from winning more trades but from preventing structural failures.

Compounding Requires Consistency

Institutional capital growth depends on consistent compounding rather than sporadic large gains.

Systems with stable behavioural characteristics and controlled drawdowns compound more reliably than those with erratic behaviour, regardless of headline performance outcomes.

Behaviour-first architecture enables this consistency. By maintaining invariant processes, measuring environmental suitability continuously, and adapting execution to observed conditions, these frameworks deliver the statistical stability that permits long-term compounding.

Implementation Requires Philosophical Realignment

Transitioning from retail to behaviour-first trading demands more than adopting new indicators or risk controls. It requires fundamental philosophical realignment about what trading systems should accomplish and how success should be measured.

Retail traders must abandon the prediction-focused mindset that views market forecasting as the primary skill. Success in behaviour-first trading comes not from predicting price movement but from maintaining structural discipline regardless of what markets do.

This transition proves difficult because behavioural discipline often means doing nothing. Retail psychology equates activity with productivity. Institutional frameworks recognize that selective inactivity—refusing to execute when behavioural criteria are not met—represents strategic advantage rather than missed opportunity.

For deeper insight into how market structure influences systematic trading decisions, explore our article on market structure analysis.

Conclusion: Behaviour Before Everything

The distinction between behaviour-first trading and retail logic extends beyond methodology into fundamental philosophy. Retail approaches treat markets as puzzles to solve through pattern recognition. Institutional frameworks treat markets as complex systems requiring continuous behavioural monitoring.

Charts provide useful information about price history. They cannot reveal structural integrity, regime stability, or environmental suitability for systematic execution. These dimensions require direct measurement of market behaviour—the foundation upon which institutional trading infrastructure is built.

Dovest’s commitment to behaviour-first principles reflects understanding that sustainable systematic trading requires prioritizing structure over prediction, integrity over excitement, and behavioural consistency over outcome optimization. Markets reward not those who predict best but those who maintain discipline when behaviour indicates danger and execute systematically when conditions align.

This philosophy guides every architectural decision, risk control, and execution parameter. Because in systematic trading infrastructure, behaviour does not come first as a preference. It comes first as a requirement.

How This Fits Dovest’s Institutional Positioning

Dovest is not a signal provider

Signals imply prediction. Dovest’s positioning is infrastructure: systematic, behaviour-first reasoning that prioritises structure, filtration, and risk architecture.

If a reader is looking for:

- “What to buy”

- “Where price is going”

- “The next breakout”

They are looking for the wrong category of system.

Dovest is not performance marketing

Behaviour-first writing intentionally avoids hype. It is built to communicate:

Why discipline is an engineering problem, not a motivation problem

How risk is defined

How constraints are enforced

How market structure affects system behaviour

About the Author

Dovest Research Team specializes in systematic trading infrastructure with focus on behavioural frameworks, market microstructure analysis, and institutional risk architecture. The team combines quantitative research with engineering discipline to develop foundational principles for structure-first trading systems.

Related published context :

- Related article: System Integrity in Trading: Why It Matters More Than Performance

- Related article: Market Structure Analysis: Why Behavior Beats Prediction

Institutional References:

- Bank for International Settlements: Market Microstructure and Liquidity Research

- CFA Institute: Systemic Risk and Market Structure