Exchange Behaviour: Why Australian, US and Hong Kong Stock Exchanges Behave Differently

Most global trading frameworks treat exchanges as interchangeable venues differentiated primarily by liquidity size or trading hours. This assumption collapses under institutional scrutiny. Exchange behaviour is not a cosmetic detail layered on top of markets—it is an emergent property of structure, regulation, participant composition, and historical design choices that fundamentally shapes how systematic trading systems must operate.

In systematic trading infrastructure, ignoring exchange behaviour leads to behavioural mismatch, execution instability, and silent risk accumulation. Markets do not merely price assets. They express identity through persistent patterns that determine how volatility forms, how liquidity responds to stress, and whether execution assumptions remain valid across regime transitions.

This article explains why exchange behaviour differs materially across the Australian Securities Exchange (ASX), US equity markets, and the Hong Kong Exchange (HKEX). Rather than viewing exchanges as neutral pipes for order flow, this framework treats them as behavioural systems with distinct personalities that systematic infrastructure must respect.

Why Exchange Behaviour Emerges From Structure

Structure Determines Response Patterns

Liquidity scale alone does not define how a market behaves under stress. Two exchanges with similar turnover can exhibit radically different responses to news, volatility shocks, and regime transitions. Exchange behaviour reflects how the market is built, not merely how large it appears on aggregate volume metrics.

Structural components shaping behaviour include market microstructure design, opening and closing auction mechanics, participant composition ratios between retail and institutional flow, regulatory intervention style, and historical volatility tolerance embedded in circuit breaker thresholds. These components interact to produce persistent behavioural patterns that systematic systems cannot optimize away.

Exchange Behaviour Governs Execution Validity

Execution assumptions valid on one exchange can fail catastrophically on another despite superficial similarity in instrument type or market capitalization. Spread stability under stress, queue dynamics during liquidity shocks, and replenishment behaviour after large trades differ fundamentally across venues.

Treating exchanges as equivalent venues forces systems to adapt behaviourally in ways that degrade integrity. Exchange behaviour therefore becomes a gating input upstream of signal logic, not a parameter to adjust during execution.

Exchange Behaviour as Market Personality

Markets express personality through repeated behavioural responses that remain stable across time even as individual instruments change. These signatures persist because they emerge from structural constraints rather than transient participant preferences.

In global systematic trading, understanding exchange behaviour answers critical operational questions: How does liquidity withdraw under different stress types? How persistent are volatility shocks relative to normal ranges? Does price discovery concentrate in continuous trading or fragment across session boundaries? How tolerant is the market structure of aggressive participation styles?

Answering these questions requires treating exchanges as behavioural entities with memory and constraint, not abstract price generators with uniform properties.

Exchange Behaviour in ASX Markets

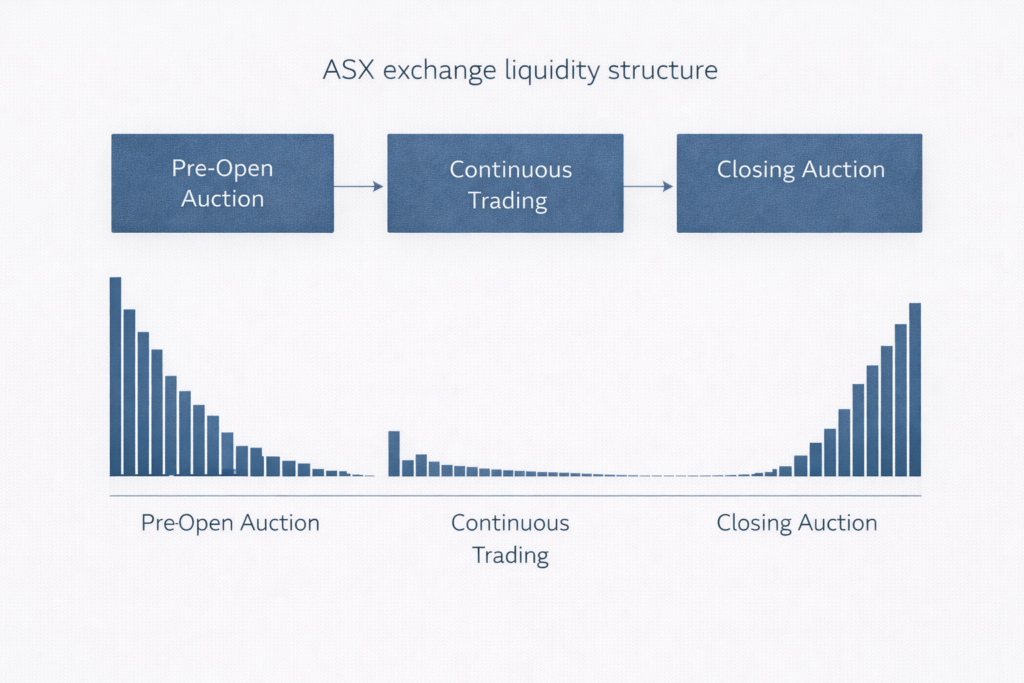

ASX Emphasizes Orderly Depth

The Australian Securities Exchange exhibits a structurally conservative personality shaped by concentrated participation and auction-centric design. Liquidity tends to concentrate in opening and closing auctions while continuous trading emphasizes orderliness over speed-competitive provision.

Key ASX behavioural traits include relatively stable spread regimes during normal conditions, slower but more predictable liquidity replenishment after large trades, strong auction-driven price discovery that dominates intraday moves, and higher sensitivity to single-stock liquidity shocks due to concentrated float.

This structure supports disciplined execution strategies but punishes aggressive intraday tactics during fragmented conditions. Systems designed for US-style continuous provision often misread ASX liquidity as deeper than it functionally is.

ASX Behaviour Under Stress Conditions

During volatility spikes, ASX liquidity often retracts unevenly rather than evaporating completely. Depth remains visible in order books but becomes fragile, leading to air pockets where mid-sized orders move prices disproportionately. Spreads widen but typically maintain some structure rather than exploding chaotically.

Systems assuming US-style continuous depth robustness during stress frequently misread these conditions as brief disruptions rather than structural regime shifts. ASX exchange behaviour rewards patience during these periods and penalizes overreaction to temporary spread widening.

Exchange Behaviour in US Markets

US Markets Prioritize Speed and Fragmentation

US equity markets represent the opposite end of the behavioural spectrum from ASX. Fragmentation across multiple venues, high-frequency participant dominance, and continuous liquidity provision define US exchange behaviour in ways that create both opportunity and fragility.

Characteristic traits include rapid liquidity replenishment under normal conditions where depth regenerates within seconds, highly competitive spread tightening driven by maker-taker economics, extreme sensitivity to regime shifts where small changes cascade quickly, and fragmented price discovery across venues that distributes risk differently than consolidated markets.

This structure enables aggressive execution during stable regimes but deteriorates rapidly when volatility regimes shift. The speed that provides advantage during normal conditions becomes a liability when liquidity providers simultaneously withdraw across venues.

US Behaviour During Regime Transitions

Under stress, US markets often exhibit sudden liquidity evaporation rather than gradual decay. Spreads widen sharply across all venues simultaneously, and adverse selection risk increases nonlinearly as informed flow concentrates. Circuit breakers trigger more frequently but provide less genuine protection due to fragmentation.

Systems that fail to adapt to US exchange behaviour during transitions often continue executing under outdated assumptions, treating temporary spread widening as noise rather than regime confirmation. The continuous provision that characterizes normal conditions can disappear within seconds during stress.

Exchange Behaviour in HKEX Markets

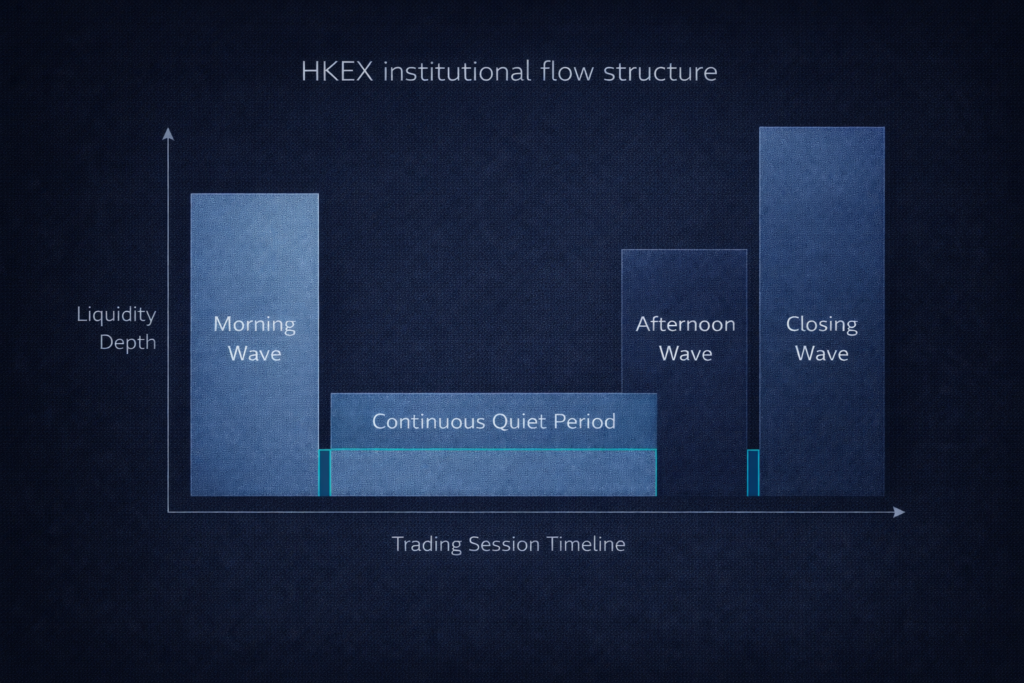

HKEX Reflects Regulatory Influence

The Hong Kong Exchange occupies a unique behavioural position shaped by strong regulatory presence, concentrated institutional flows from mainland China, and cross-border participation dynamics. HKEX exchange behaviour differs from both ASX conservatism and US fragmentation.

Key characteristics include discrete liquidity waves driven by institutional flow timing rather than continuous provision, pronounced opening and closing effects that dominate daily volume distribution, higher tolerance for gap risk embedded in circuit breaker design, and structural sensitivity to macro-political signals that affect cross-border capital flows.

Market structure accommodates sudden participation changes rather than smoothing them, creating step-function liquidity patterns instead of gradual transitions.

HKEX Volatility Behaviour Patterns

Volatility on HKEX often manifests as step changes rather than smooth diffusion processes. News impact creates discrete repricing events with gap risk rather than continuous adjustment. Systems expecting gradual volatility decay frequently misclassify regime state because the market structure does not support mean reversion assumptions.

HKEX exchange behaviour rewards structural alignment with these patterns over responsive adjustment. Attempting to trade through gaps or fade apparent overreactions often compounds losses because the exchange structure reinforces rather than dampens directional moves.

Comparing Exchange Behaviour Across Regions

Liquidity Behaviour Differences

Exchange behaviour manifests distinctly in how liquidity appears, responds, and withdraws across ASX, US markets, and HKEX. ASX exhibits concentrated, auction-centric liquidity that pools at session boundaries rather than distributing evenly throughout continuous trading. US markets demonstrate continuous, fragmented liquidity that exists across multiple venues simultaneously but can evaporate rapidly across all venues during stress.

HKEX displays episodic, institution-driven liquidity that arrives in waves tied to participant timing rather than continuous market-making obligations. These differences persist because they emerge from structural design rather than transient preferences.

Volatility Personality Differences

How volatility forms and dissipates differs fundamentally across exchanges. ASX typically exhibits contained, mean-reverting shocks where single-stock moves remain bounded by concentrated float dynamics. US markets show regime-sensitive, shock-amplifying volatility where initial moves can cascade through fragmented venues.

HKEX demonstrates discontinuous, event-driven volatility where gaps dominate adjustment processes. Understanding these personalities prevents systems from applying uniform volatility models across regions.

Exchange Behaviour and Filtration Logic

Exchange behaviour directly informs filtration logic in systematic trading infrastructure. A market structure validation that passes on one exchange may fail on another purely due to behavioural mismatch, not fundamental opportunity differences.

For example, a volatility regime acceptable on ASX where mean reversion dominates may invalidate execution on US markets where regime shifts cascade quickly. Similarly, liquidity conditions tolerable on HKEX where discrete waves are normal may represent structural danger on ASX where continuous depth is expected.

Filtration logic systematic trading must incorporate exchange behaviour as a first-class gating input rather than treating it as an execution-layer parameter.

Exchange Behaviour and Downside Risk

Downside risk manifests differently across exchanges based on structural behaviour patterns. Systems that apply uniform downside models across venues ignore how exchange behaviour shapes tail risk formation and propagation.

ASX downside often arrives through liquidity thinning where visible depth becomes fragile but does not disappear completely. US downside arrives through sudden fragmentation where liquidity evaporates simultaneously across venues. HKEX downside arrives through discontinuous repricing where gaps create realized losses before protective mechanisms activate.

Understanding downside-focused risk architecture requires exchange-specific behavioural calibration rather than universal threshold application.

Exchange Behaviour and Data Trust

Data trust frameworks must also adapt to exchange behaviour differences. Historical data stability varies by exchange based on structural changes, regulatory interventions, and participation evolution. Reconstructing behavioural baselines without accounting for exchange identity leads to leakage and false confidence in backtest results.

ASX data exhibits relative stability due to structural conservatism. US data requires careful handling of venue fragmentation changes over time. HKEX data must account for regulatory regime shifts that alter participation rules.

Exchange-aware data trust systematic trading preserves causal integrity by respecting these structural differences.

Institutional Research on Exchange Behaviour

Institutional research emphasizes that market quality and liquidity provision are conditional properties dependent on structure, not guaranteed features of all venues. According to research from the Bank for International Settlements, liquidity behaves fundamentally differently across market structures, particularly during stress periods when structural differences dominate outcomes.

The CFA Institute highlights how microstructure differences create persistent behavioural patterns that systematic trading infrastructure must respect. These patterns remain stable over time because they emerge from foundational design choices rather than temporary participant preferences.

Exchange Behaviour as Design Constraint

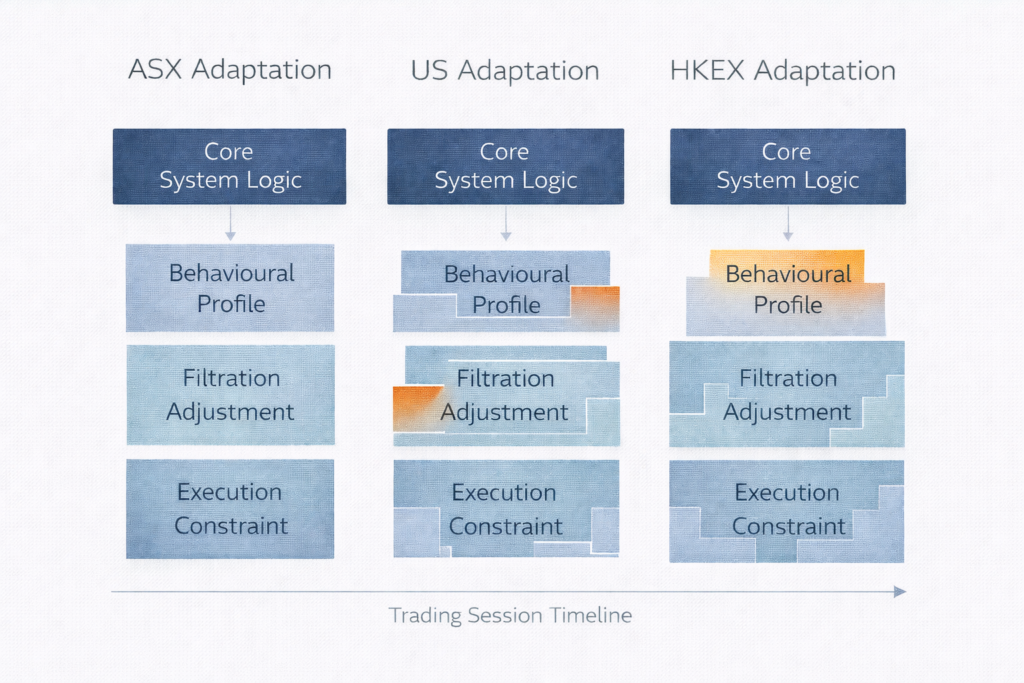

Global systematic systems fail when they attempt to normalize markets by treating structural differences as noise to filter out. Exchange behaviour resists normalization because it emerges from architectural constraints that no amount of optimization can overcome.

This reality requires global infrastructure to incorporate exchange-specific behavioural profiles that shape how systems interpret conditions, venue-aware filtration logic that adapts gating criteria to structural realities, and regionally adaptive execution constraints that respect rather than fight local market personality.

Ignoring exchange identity creates behavioural debt that surfaces during regime shifts when structural differences dominate outcomes. Systems designed for one exchange behaviour often fail catastrophically when deployed to venues with different personalities.

Why Exchange Behaviour Is Not Arbitrage Opportunity

Exchange behaviour differences do not represent inefficiencies to exploit through cross-venue arbitrage. They represent constraints to respect through structural alignment. Attempting to arbitrage behaviour across exchanges without accounting for structural differences often amplifies risk rather than capturing edge.

For example, attempting to exploit ASX-US volatility differences by assuming mean reversion works similarly on both venues ignores that US fragmentation creates different shock propagation dynamics. The apparent opportunity typically reflects insufficient understanding of structural constraints rather than genuine mispricing.

Designing for Behavioural Consistency

Systems that scale globally do not behave identically everywhere. Instead, they behave consistently relative to exchange behaviour by adapting to local structural realities while maintaining core principles.

Consistency emerges from structural alignment with local market personality, behavioural compatibility between system assumptions and venue characteristics, and execution discipline that respects rather than fights local constraints. Universal logic applied uniformly across venues creates fragility.

Exchange Behaviour Defines Market Reality

ASX ≠ US ≠ HKEX because markets are not abstract price generators with interchangeable properties. They are behavioural systems with identity, memory, and structural constraints that shape every aspect of systematic trading execution.

Exchange behaviour determines whether execution is earned or denied based on structural compatibility, whether risk remains bounded or compounds silently through behavioural mismatch, and whether systems preserve integrity across regime transitions or degrade when structural assumptions break.

Global trading infrastructure scales not by predicting markets or normalizing differences, but by respecting the behavioural rules each exchange enforces implicitly through structure. Systems that attempt to impose uniform logic across venues accumulate behavioural debt that surfaces as unexplained degradation during stress periods.

Understanding exchange behaviour as emergent property rather than cosmetic detail enables infrastructure design that aligns with rather than fights structural reality. This alignment protects system integrity by ensuring behavioural compatibility remains intact across all operational venues.

Continue Learning About Systematic Behaviour Frameworks

Explore more research on behaviour-first infrastructure design and exchange-specific systematic trading architecture.

About the Author

This article was developed by Dovest’s systematic trading research team. Our work focuses on behaviour-first infrastructure design, structural risk management, and exchange-specific architectural principles that enable consistent systematic trading execution across global markets. We specialize in translating institutional trading research into practical framework implementation, with particular emphasis on exchange behaviour analysis and regional market structure differences.

Our research draws on market microstructure analysis, comparative exchange architecture studies, and decades of institutional trading infrastructure development across ASX, US, and Asian markets. We maintain strict separation between theoretical framework and performance claims, focusing exclusively on structural design principles.

Disclaimer

This article provides educational information about exchange behaviour and market structure differences across global venues. It does not constitute financial advice, investment recommendations, or trading signals. Exchange behaviour patterns discussed reflect historical structural characteristics that may change due to regulatory modifications, technological evolution, or participant composition shifts.

Systematic trading involves substantial risk including potential loss of capital. No framework guarantees profitable outcomes or eliminates trading risk across any exchange. Past behavioural patterns do not guarantee future structural consistency. Readers should conduct independent research and consult qualified financial professionals before implementing systematic trading strategies on any venue.

Dovest provides research and educational content about systematic trading infrastructure and exchange behaviour. We do not offer investment advice, manage client assets, or guarantee trading outcomes. All content reflects current research and may be updated as frameworks evolve.